Implementing Ordinance of the Federal Council on Swiss Derivatives Trading Rules Published

On 25 November 2015 the Federal Council released the final version of its implementing ordinance (“FMIO”) to the Swiss Financial Markets Infrastructure Act (“FMIA”). The FMIO provides for important clarifications and implementation provisions for, among other things, the new rules on derivatives trading provided for by the FMIA (including clearing, reporting and risk mitigation obligations). The FMIA and the implementing ordinances are expected to become effective on 1 January 2016, subject to a phase-in.

By Stefan Kramer (Reference: CapLaw-2015-57)

1) Introduction and Background

The FMIA aims to implement the G-20 reform agenda regarding over-the-counter (OTC) derivatives markets and to create a regulation equivalent to the European Union’s European Market Infrastructure Regulation (EMIR). The FMIA requires counterparties to OTC derivatives transactions to comply with a variety of obligations (including clearing, reporting and risk mitigation obligations), which apply not only to so-called financial counterparties (such as banks and insurance companies), but also to non-financial counterparties (such as trading and industrial companies). Given the technical nature of most of its provisions and the desire to create a flexible set of rules that can be quickly amended to reflect changes to international market standards, the FMIA takes the form of a framework legislation. Accordingly, the FMIA provides for a wide delegation of powers to the Federal Council and FINMA to enact implementing ordinances.

2) Certain Key Aspects of the FMIO

a) Thresholds for Counterparty Categorization

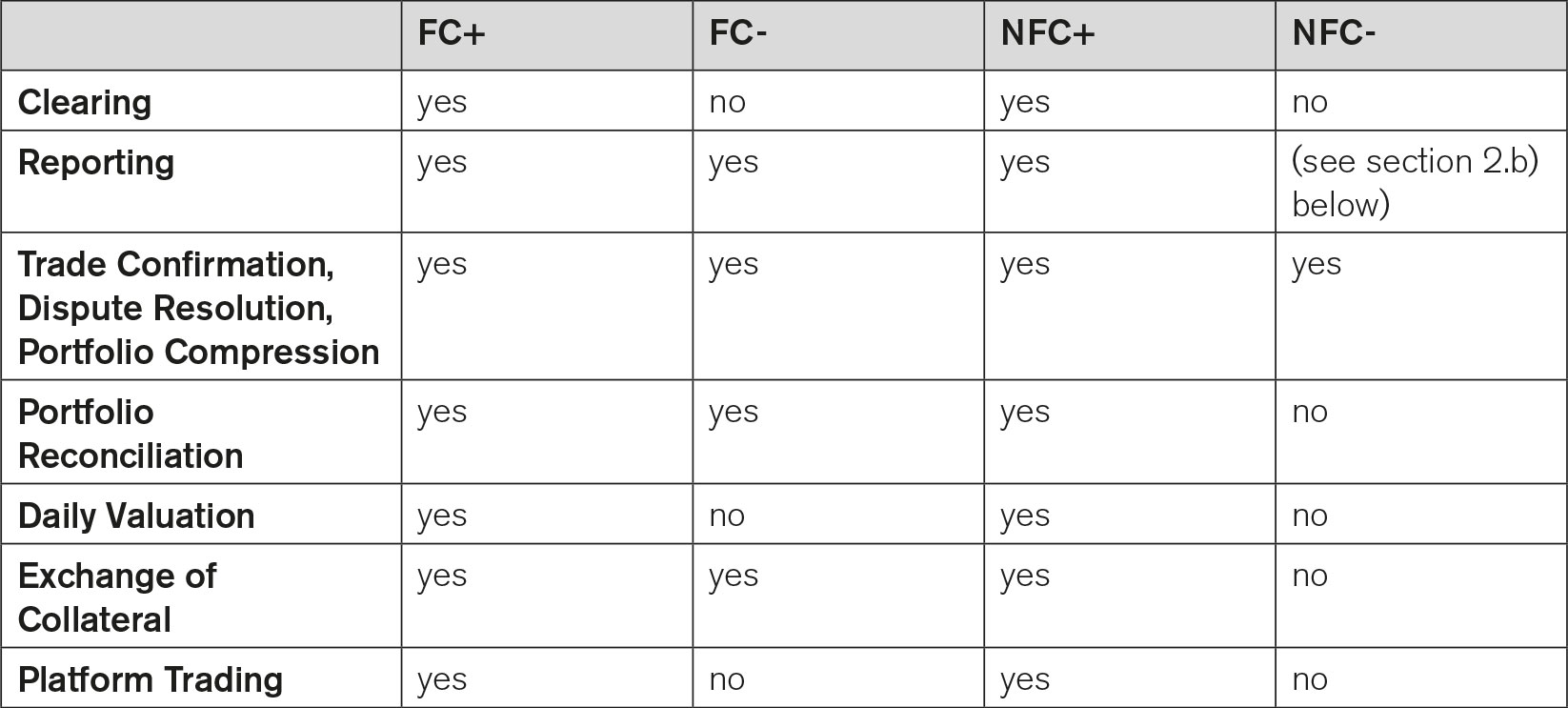

In terms of an overview, the obligations under the FMIA apply to the following categories of counterparties:

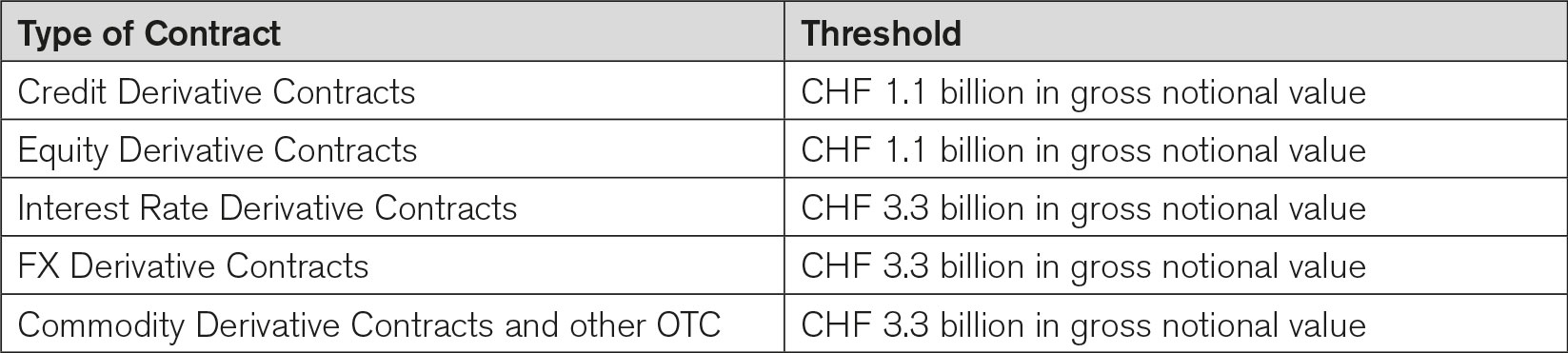

A non-financial counterparty (NFC) is deemed to be a small non-financial counterparty (NFC-) if its average gross position of outstanding OTC derivative contracts calculated on a rolling basis over 30 working days is below the applicable threshold in each of the following categories (subject to certain exclusions, e.g., in relation to hedging transactions):

A financial counterparty (FC) is deemed to be a small financial counterparty (FC-) if its aggregate average gross position in all outstanding OTC derivative contracts calculated on a rolling basis over 30 working days is below the threshold of CHF 8 billion on a financial group level. Counterparties that are not small are hereinafter referred to as FC+ or NFC+, respectively.

The FMIO further provides that thresholds are generally to be calculated by taking into account derivative contracts entered into by fully consolidated group companies. However, with a view to avoid any unnecessary deviations from the calculation of thresholds under EMIR, we believe that the Swiss rules should be interpreted to only require non-financial counterparties to include contracts entered into by other non-financial entities within the same group, and financial counterparties to include contracts entered into by other financial entities within the same group.

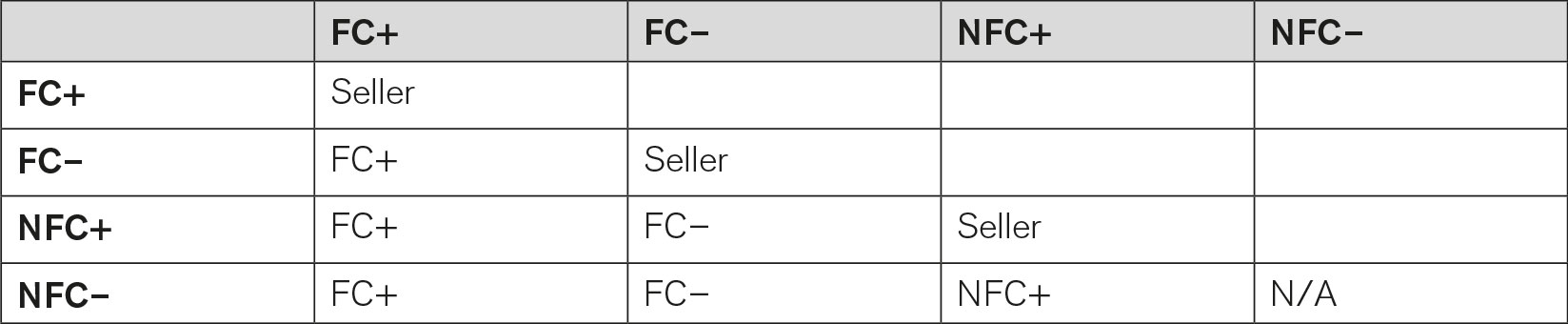

b) Allocation of Reporting Obligation

The FMIA introduces an obligation to report all new, modified or terminated derivative contracts to an authorized or recognized trade repository. The duty to report is generally allocated to one party to the transaction (one-sided reporting). Transactions between two small non-financial counterparties are exempt from the reporting obligation (but an NFC- may still be required to report trades with a non-Swiss counterparty if the non-Swiss counterparty does not itself report the trade). The reporting obligation is generally allocated as follows:

If the transaction is cleared centrally, the report shall be submitted by the central counterparty. If a recognized foreign central counterparty does not submit a report, the reporting duty shall remain with counterparties. Subject to the CCP’s duty to report, centrally cleared exchange traded derivatives have to be reported by the counterparty whose position is closer to the central counterparty in the transaction chain.

c) Thresholds for Portfolio Reconciliation | Portfolio Compression

As a general rule (with the exception of OTC derivative contracts with an NFC–), counterparties must have in place procedures for periodic portfolio reconciliation. The periodicity of the periodicity of the portfolio reconciliation depends on the number of OTC Derivative contracts outstanding (not including FX swaps and forwards):

![]()

In addition, counterparties must regularly, but at least twice per year, perform portfolio compression if they have 500 or more non-centrally cleared OTC derivative contracts outstanding, except if (i) this is not expected to lead to a limitation of counterparty risk (e.g., because the portfolio contains no or only a small number of offsetable transactions), and|or (ii) the effort would be disproportionate to the expected reduction of the counterparty credit risk.

d) Cross-border Transactions | Availability of “Substituted Compliance”

As a general rule, transactions between a Swiss counterparty and a counterparty domiciled abroad are subject to the provisions of the FMIA regarding clearing, reporting and risk mitigation obligations. However, the Swiss rules provide for a substituted compliance regime and certain exemptions with a view to avoid duplicative or conflicting rules in case of cross-border transactions:

The Swiss rules provide for substituted compliance regime in that a counterparty may satisfy its obligations under the FMIA by complying with foreign regulations, if (i) the relevant foreign law is recognized as being equivalent (FINMA will recognize foreign law as being equivalent if the obligations regarding derivative transactions as well as the provisions regarding supervision are in their material effects comparable to the corresponding Swiss provisions), and (ii) with respect to clearing and reporting obligations, if the relevant foreign central counterparty (CCP) or trade repository has been recognized by FINMA (or has been exempted from the recognition requirement by FINMA) (c.f., section 2.e) below).

In addition, the FMIO provides for an exemption from the clearing obligation and the obligation to exchange collateral, as applicable, for cross-border transactions with a third country entity which (i) has its registered office in a third country whose law is recognized as being equivalent by FINMA, and (ii) is not subject to a clearing obligation or the obligation to exchange collateral, as applicable, pursuant to the laws of the relevant country.

e) Recognition of Foreign CCPs and Trade Repositories

The clearing obligation and reporting requirements under the FMIA may be satisfied by Swiss market participants using a foreign CCP or trade repository, as applicable, which has been recognized by FINMA (c.f., section 2.f) above). FINMA shall grant recognition for a foreign CCP or trade repository if:

- the foreign CCP | trade repository is subject to appropriate regulation and supervision; and

- the competent foreign supervisory authorities:

- do not have any objections to the cross-border activity of the foreign CCP | trade repository,

- confirm that they will inform FINMA if they detect violations of the law or other irregularities on the part of Swiss participants, and

- provide FINMA with administrative assistance (in case of CCPs) or certain guarantees in relation to the access to, and the use of, data collected (in case of trade repositories).

FINMA may refuse recognition if the state in which the foreign CCP | trade repository has its registered office does not grant Swiss CCPs or trade repositories, as applicable, actual access to its markets or does not offer them the same competitive opportunities as are granted to domestic central counterparties | trade repositories. Any international commitments to the contrary (e.g., GATS) are reserved.

FINMA may exempt a foreign CCP from the obligation to obtain recognition, provided this does not interfere with the protective purpose of the FMIA.

Recognition of a trade repository may be based on a general determination by FINMA in relation to a particular jurisdiction confirming that the relevant foreign regulation and authorities satisfy the requirements of the FMIA.

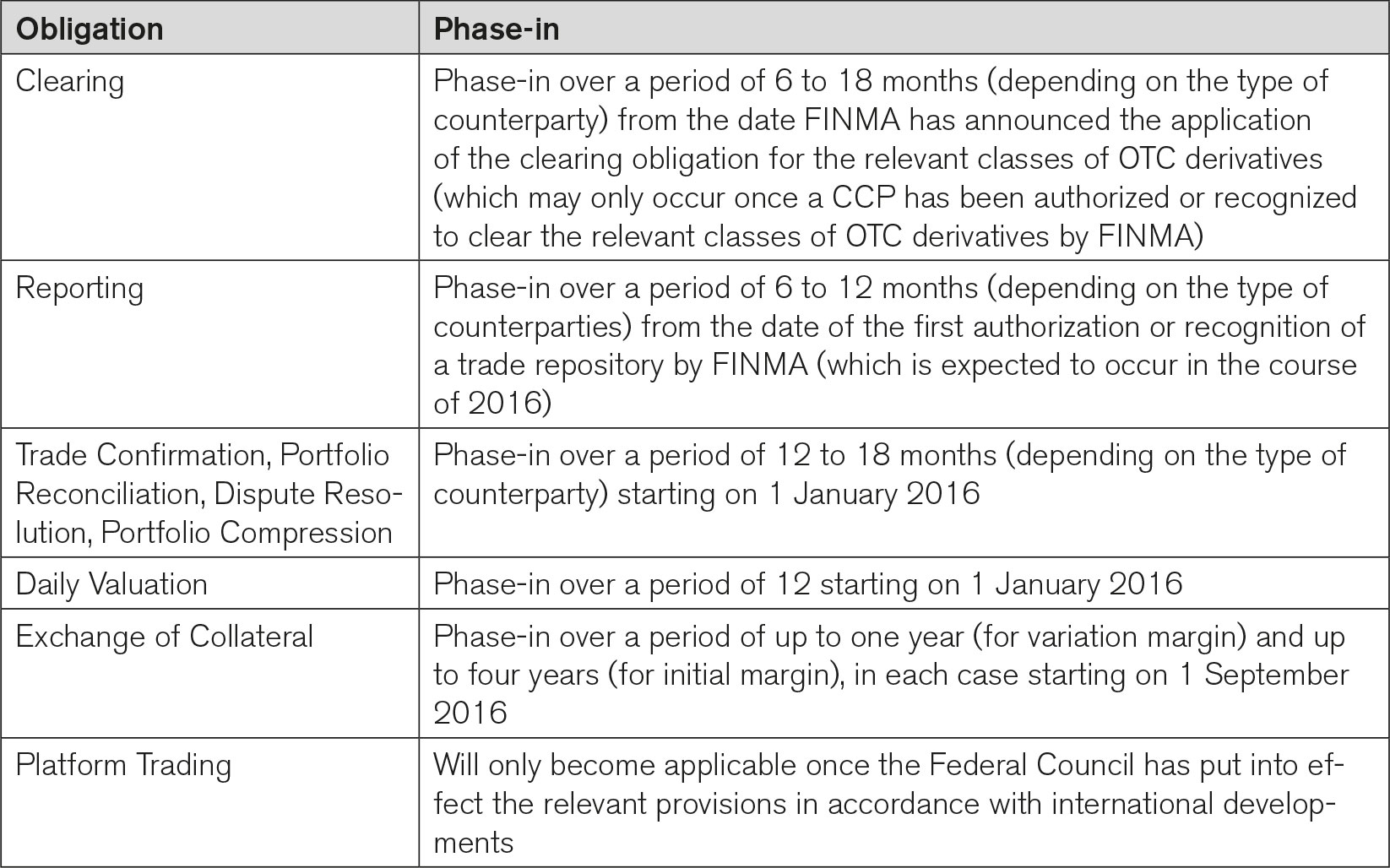

f) Timing of Application | Phase-in Periods

The FMIO provides for the following phase-in periods (which may be extended by FINMA under certain circumstances):

3) Outlook

According to a press release of the Federal Council of 25 November 2015, the FMIA and the FMIO will become effective on 1 January 2016, subject to the aforementioned phase-in periods.

Stefan Kramer (stefan.kramer@homburger.ch)