Partial Revision of the Swiss Insurance Supervision Ordinance

The partial revision of the Swiss Insurance Supervision Ordinance (ISO) initiated by the Federal Finance Department (FFD) in 2014 will enter into force on 1 July 2015. The revision focuses primarily on the themes of solvency, qualitative risk management and disclosure. This article shall give an overview on the various amendments, and in particular on the revised provisions on the eligibility of hybrid instruments as regulatory capital.

By Petra Ginter (Reference: CapLaw-2015-18)

1) Introduction

The necessity to revise the insurance supervision law became evident in the financial crisis. Furthermore, the introduction of the risk-based Swiss Solvency Test (SST), the equivalence assessment by the European Insurance and Occupational Pensions Authority (EIOPA) in autumn 2011, the Financial Sector Assessment Program (FSAP) of 2013, as well as other international developments, led to the conclusion that a revision of the ISO would be inevitable.

As mentioned, the primary focus of the amendments to the ISO lies on solvency, qualitative risk management and disclosure. At the same time, adjustments will be made to insurance technical reserves, tied assets, intermediary supervision and certain sector-specific provisions.

2) Solvency

a) Discontinuation of Solvency I

The current ISO requires (re)insurance companies to apply two equivalent solvency methods: Solvency I as well as SST. The latter has been applied to Swiss domiciled (re) insurance companies and groups since 2011 by operation of law.

To apply two solvency methods in parallel is, however, no longer considered adequate and also not in line with international standards. Already the message of the Swiss Federal Council (Botschaft) on the Insurance Supervision Act (ISA) of 2003 stated that the solvency margins calculated under Solvency I would not provide the necessary protection because Solvency I would not take into account the individual risk profile of the (re)insurance company. Under Solvency I, the required capital is determined based on the volume of the business by applying volume related, formalistic standard calculations. The method does not request higher capital requirements for companies with higher risks and does not take into account market and credit risk. Accordingly, the Solvency I method was considered of limited relevance and was said to barely support the main goal of insurance supervision regulation, namely the protection of the insured. Considering these shortfalls of the Solvency I method, it lost its relevance after the SST became mandatory, even more as today’s insurance supervision is a risk-based supervision. Finally, on the EU level, the Solvency I method will be replaced as per 2016 by the new solvency regime under the Solvency II Directive 2009/138/EG (Solvency II).

As a consequence, Solvency I will be discontinued under the revised ISO and the SST will be applied as the sole solvency method and as counterpart to the new Solvency II method in the EU. The SST allows – with a few exceptions – a holistic view on the risks of the (re)insurer and the resulting capital requirements, assessed close to market. The relevant market, credit and insurance risks will be quantified by means of a standardised or individual model and the resulting capital requirements (target capital) will be compared to the effectively available capital (risk-bearing capital). The discontinuation of Solvency I will become effective as per the entering into force of the revised ISO, i.e. as per 1 July 2015. In essence, no transitional rules will be applied with respect to the application of Solvency I.

Under the revised ISO, Solvency I will only continue to be applied if an international treaty requires such application. The relevance of this exemption is limited to casualty insurers pursuant to the treaty between Switzerland and the European Union on casualty insurance (SR 0.961.1).

b) Preference of SST Standard Models

Today, around half of the (re)insurance companies that are subject to SST requirement have developed their own internal models. The remaining (re)insurance companies assess their regulatory solvency requirements by applying FINMA’s standard model.

On the one hand, practice has shown that a sound review of sophisticated internal models requires overly extensive efforts by the regulator. On the other hand, developing and maintaining an internal model also results in substantial efforts and costs for the (re)insurance company in order to comply with the regulatory requirements. Therefore, the practical application of SST will be adjusted in the interest of a commercially reasonable use of resources. This goal will predominantly be achieved by preferring the use of standard models over the individual models. In addition to simplifying the application, the preferred use of standard models will also result in the ability to better compare market participants’ solvency positions.

With the revised ISO, the preference of standard models over individual models will be established. It is, however, not the expressed intention of the regulator to thereby apply higher capital requirements in the insurance market. The revised ISO provides for sufficient transitional rules with respect to the application of the respective models.

3) Qualitative Risk Management

Qualitative risk management refers to the non-financial performance, i.e. organisation, structure and processes of the (re)insurance company. In particular, the revised ISO sets forth stricter requirements for risk management as well as for corporate governance, including the separation of power between the board of directors and executive management, control functions and compliance. Risk management and compliance functions must be independent and need to be staffed according to size, business and organisational complexity and risks.

The current rules under the ISO are considered to be too generic and limited to a few rules which do not fulfil the international standards of the Insurance Core Principles of the International Association of Insurance Supervisors (IAIS ICPs). This has been identified by the latest FSAP review.

The revised ISO will also introduce specific requirements for an Own Risk and Solvency Assessment (ORSA) which the current ISO lacks completely. ORSA requires at least a yearly forward-looking self-assessment of the risk situation and capital requirements, including reporting requirements to FINMA. The overall risk profile shall thereby reflect all risks the (re)insurance company is and may be exposed to, including all significant risk concentration and group-wide risks.

Finally, the revised ISO will also provide a proper legal basis for applying specific liquidity requirements. The (re)insurance company needs to have sufficient liquidity in order to fulfil the payment obligations at any time, including in stress situations. The liquidity assessment will also include adverse scenarios and respective stress tests as well as an emergency concept, including effective strategies to deal with liquidity constraints. The already existing FINMA Circular 13/5 Liquidity Insurers does, however, only include liquidity reporting duties. Following the implementation of the new ISO liquidity requirements, the FINMA Circular 13/5 Liquidity Insurers will need to be amended accordingly.

4) Disclosure and Reporting

Under the current ISO, FINMA does not publish solvency results of individual (re)insurance companies. The revised ISO contains a disclosure concept which will be equivalent to internationally accepted standards (IAIS ICPs and Solvency II). The new ISO rules will provide an explicit legal basis in order to establish a direct disclosure on the level of the ISO. With a view to avoid competitive disadvantages, the revised ISO disclosure regime will not become effective prior to Solvency II coming into force.

The revised ISO will further include a new article on the requirement to publish an annual report on the financial situation of the (re)insurance company (article 111a ISO). Such report will include quantitative and qualitative information, and in particular, a description of the business activity, company success, risk management and adequacy, risk profile, valuation basis and methods in particular with respect to reserves and solvability.

Finally, the draft ISO will include stricter, i.e. earlier, requirements for the disclosure of substantial participations for (re)insurance groups as per the time of a respective intention to create, acquire and sell such substantial participations by one of its group companies (article 192(2) ISO) and the reporting of intragroup transactions to FINMA prior to them becoming legally binding (article 194(2) ISO).

5) New Hybrid Regime

a) Capital Treatment of Hybrid Instruments

A significant benefit for (re)insurance companies which are active in the hybrid market will be the more flexible rules on the treatment of hybrids for regulatory capital purposes.

(Old) article 39 ISO on “hybrid instruments” will be replaced by (new) article 22a ISO on “risk absorbing capital instruments” defining the requirements for debt instruments to be eligible for Solvency I and SST. The broader term “risk absorbing capital instruments” will not only include debt instruments that are paid-in from inception, but also instruments which become statutory equity upon reaching a pre-defined trigger. E.g. upon reaching an SST ratio under 100%, such instruments will be written off or converted into common shares, hence becoming statutory equity.

Risk absorbing capital instruments are accountable as statutory capital under Solvency I provided they fulfil all criteria set forth in (new) article 39(1)(a)-(g) ISO. For convertible debt instruments, the conversion from debt to equity only happens upon reaching a certain trigger event. Consequently, such instrument may influence the risk bearing capital in a year and thus should be eligible to be accounted as reduction of the SST target capital. The eligibility requirements are largely unchanged, however, the following three key changes will be introduced:

- debt instruments that qualify under article 22a ISO can either be eligible as available capital under Solvency I and SST, or as a reduction in required capital under SST;

- not only subordinated debt instruments qualify but also debt instruments that convert into statutory equity upon a contractual trigger; and

- FINMA has the authority to define additional requirements for risk absorbing capital

instruments to be eligible, such as criteria on the quality of the instruments.

The approval for recognising risk absorbing capital instruments as available capital (Solvency I) will, under the revised rules, also be required for recognition in the risk bearing or the target capital (SST).

b) Key Changes to Limits

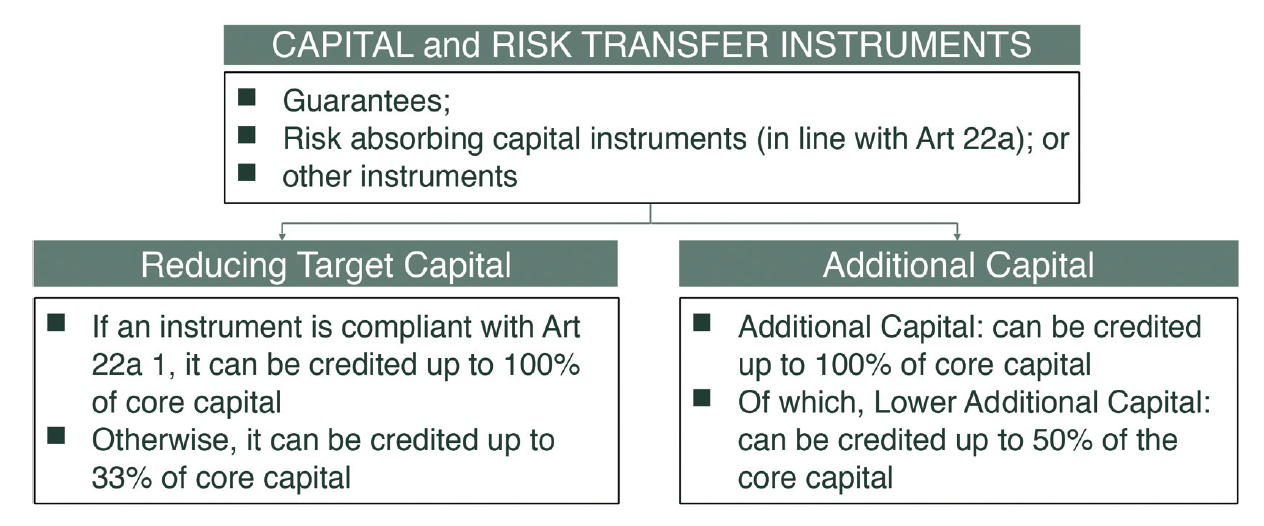

The Solvency I limits remain unchanged. I.e., perpetual risk absorbing instruments can be accounted up to 50% of the lower of the available or required capital. Dated risk absorbing instruments are allowed up to 25% of the lower of the available or required capital.

The SST limitations for upper and lower additional capital instruments also remain unchanged. Additional capital instruments recognised as part of risk bearing capital (available capital) are allowed up to 100% of core capital. Lower additional capital (dated debt instruments) is allowed up to 50% of core capital.

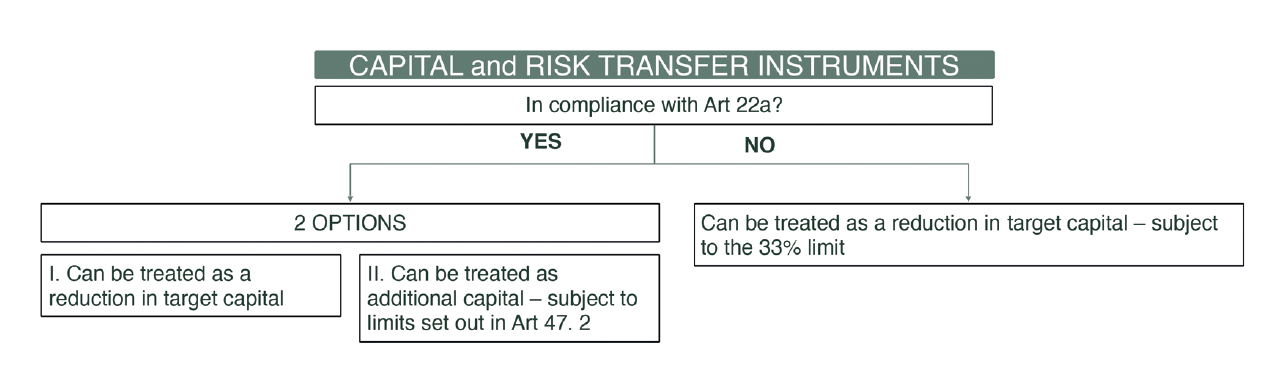

The revised ISO provisions provide, however, for new additional SST hybrid limitations. The overall limit for risk absorbing capital instruments as defined in (new) article 22a ISO is up to 100% of core capital for their consolidated impact on available or required capital. Capital and risk transfer instruments that are not in compliance with (new) article 22a ISO can be accounted as reduction of required capital up to 33% of core capital.

6) Next Steps

In line with the revised ISO, FINMA will continuously develop and communicate its supervisory practice. While a number of FINMA circulars will be adjusted, new circulars will also be drafted until 1 January 2017.

Petra Ginter (Petra_Ginter@swissre.com)