Funds Distribution under the new financial market law architecture

On 1 January 2020, the new Financial Services Act (FinSA) and the Financial Institutions Act (FinIA) will enter into force. This entails various changes of existing regulatory concepts in the context of distribution and management of collective investment schemes. From today’s CISA perspective, the term “distribution” under Art. 3 CISA plays a fundamental role. Under the new regulatory regime, an exclusive focus on the new concept of the offer falls short in explaining the rules governing the distribution of funds. Particularly with regard to the behavior at the point of sale, the concept of financial services is of primary importance.

By Diana Imbach Haumüller / François Rayroux (Reference: CapLaw-2019-56)

1) Introduction

a) The new financial market law architecture

On 1 January 2020, the new Financial Services Act (FinSA) and the Financial Institutions Act (FinIA) will enter into force and will subject, as a result of this legislative change, the existing financial market law architecture to sweeping reforms. Today, the management and distribution of collective investment schemes are governed by the Collective Investment Schemes Act (CISA) and its implementing ordinances, FINMA Circulars as well as SFAMA self-regulations. Under the new legal framework, most of this sectorial regulation will be included into laws, horizontally applicable across sectors, to all financial instruments and financial service providers. This entails various changes of existing regulatory concepts in the context of distribution and management of collective investment schemes.

b) Impact of the new legal framework on collective investment schemes

The CISA currently governs three different areas: (i) the licensing and supervision of financial institutions in relation to collective investment schemes, (ii) the distribution of collective investment schemes and (iii) the approval of collective investment schemes as well as other product-specific rules relating to collective investment schemes.

i. Licensing and supervision of financial institutions

Under the new financial market legislation architecture, the licensing and supervision of fund management companies and fund managers will be governed comprehensively by the FinIA. The corresponding provisions are to be largely transferred unchanged from the CISA. Fund managers and external managers of pension funds will be collectively known as “managers of collective assets”.

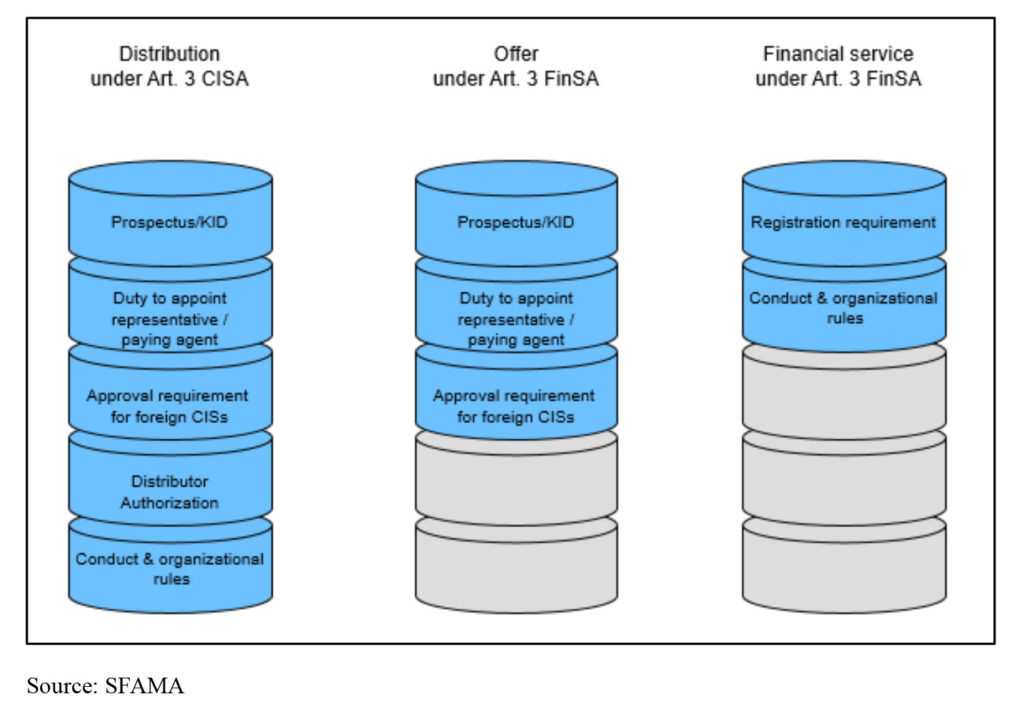

ii. Distribution of collective investment schemes

The rules regarding the distribution of collective investment schemes, as well as the related rules for the provision of financial services, will be governed by the FinSA. This means, among other things, that the current term “distribution” (Art. 3 CISA) will be abandoned in favor of the “offering”, the provision of a “financial service” respectively (see chart below). This implies fundamental changes. In particular, distributors will no longer require a FINMA license. However, this will be offset by a new prudential supervision of all asset managers, as well as by the registration requirement for client advisers under the FinSA. Ultimately, the FinSA will impose the obligation to comply with a set of rules of conduct at the point of sale in connection with all financial instruments and services. The corresponding CISA rules (Arts. 10 and 20 et seq. CISA) will therefore be limited to product-specific aspects and cease to impose specific fund related conduct and organizational rules at the point of sale. Rules pertaining to product documentation, i.e. the prospectus requirement and the rules on the production of a KID for retail clients, will also essentially be governed by the FinSA.

iii. Approval of collective investment schemes and other product specific rules

Only product-specific rules will remain in the CISA. This includes rules on contractual investment funds, which constitute the vast majority of Swiss funds, SICAVs, SICAFs, limited partnerships for collective investments as well as the duty to obtain approval from FINMA for foreign funds offered to non-qualified investors in Switzerland, and the duty to appoint representatives and paying agents. With the introduction of the FinSA and the FinIA, a significant change will be the limitation of the obligation to appoint a Swiss representative and paying agent to collective investment schemes targeting investors that are not “per se” qualified investors.

c) The abolition of the term “distribution”

Under today’s CISA, the term “distribution” under Article 3 CISA plays a fundamental role (for a detailed discussion of the term “distribution”, see Imbach/Rayroux, Funds distribution under FinSA/FinIA: A change of paradigm, CapLaw 5/2018, p. 42 et seqq.)

On the one hand, this notion is relevant to assess whether the product-specific approval requirements for foreign collective investment schemes (Art. 120 CISA) and the duty to appoint a representative and a paying agent (Art. 120 para. 4 CISA) apply. Further, the requirement to provide certain fund documents, such as a prospectus or a KID, is closely linked to the term “distribution” or “distribution to non-qualified investors”, respectively. All these aspects will be governed by the definition of the term “offering” under Article 3 let. g FinSA in the future. On the other hand, today, the term distribution also triggers the application of the conduct and organizational rules of the CISA, as well as the duty to obtain a distributor license from FINMA. In the future, these aspects will be governed by the new concept of “financial service”. The definition of this term under Article 3 let. c FinSA will be essential to determining whether the organizational and conduct rules of FinSA apply as well as whether the affiliation with an Ombudsman and the registration in the new client advisor registry are required

Against this background, it becomes obvious that an exclusive focus on the new concept of the offer falls short in explaining the rules governing the distribution of funds under the new regulatory framework of FinSA. In particular with regard to the behavior at the point of sale, the concept of financial services is of primary importance.

d) Challenges and perspectives

It was a conscious choice of the legislator to abolish not only the conduct and organizational rules deriving from the concept of a distribution under CISA, but also the distributor license under Art. 13 para 2 lit. g CISA. Based on the explanations above under section c), this only makes sense from a CISA perspective if a number of circumstances, which today constitute a distribution of funds, are classified as a financial service under FinSA, even where such circumstances do not imply a transaction-related advice. One has also to see the need for this construction of the concept of a financial service against the background of the abolition of the obligation to appoint a representative in dealings with “per se” qualified investors (Art. 120 para. 4 CISA) which is responsible for ensuring that foreign fund providers and distributors comply with the rules of conduct. In other words, the aim was not to create a gap in the existing rules for the protection of investors, but to ensure that the discontinued CISA rules shall be adequately integrated in the new FinSA regulations. This was the main driver of the authors of the legislative texts specified in Article 3 para. 1 of the FinSO draft from October 2018 and thereafter in Article 3 para. 2 of the final version of FinSO together with and explanatory comment in the final Explanatory Report of the Federal Finance Department, p. 19 (Explanatory Report).

However, since FinSA applies not only in the context of collective investment schemes, but to all financial instruments and financial services according to FinSA, it was particularly important to consider specific aspects in relation with other financial instruments and services. Against this background, the definitions of the concept of a financial service, as well as of the offer, were narrowed and specified in the final version of FinSO in line with the intent of the legislator not to introduce a new financial markets regulation which is more stringent than necessary to ensure an appropriate level of investor protection considering existing regulation. Therefore, the FinSO expressly clarifies among others that any advice in relation to financing or capital market transactions, as well as M&A activities and related services, do not constitute financial services within the meaning of Article 3 let. c FinSA (Article 3 para. 3 FinSO) (for further details see section 2) below).

Moreover, from a CISA perspective, a few clarifications were important (for an extensive overview see SFAMA’s and Lenz & Staehelin’s responses during the consultation process for FinSO and FinIO). One of the most important was the clarification under Article 3 para. 2 FinSO that, in order to be characterized as a financial service according to Article 3 let. c ciph. 1 FinSA, there must be a contact of a financial services provider with an end-investor. Hence, the provision of information on financial instruments to supervised financial intermediaries is generally not regarded as a financial service within the meaning of this provision (see Explanatory Report, p. 19).

2) Fund distribution as a financial service

a) Financial Services

i. Definition

Article 3 let. c ciph. 1 FinSA includes a conclusive list of financial services, namely (1) acquisition or disposal of financial instruments, (2) receipt and transmission of orders in relation to financial instruments, (3) administration of financial instruments (portfolio management), (4) provision of personal recommendations on transactions with financial instruments (investment advice), and (5) granting of loans to finance transactions with financial instruments. As mentioned above, from a fund perspective, it is clear that many circumstances, which today constitute a distribution of collective investment schemes, are to be characterized as a financial service pursuant to Article 3 FinSA. In addition, the Dispatch of the Federal Council, dated 4 November 2015, stated that “classic” fund distribution – outside of an advisory or asset management agreement – must also be characterized as a financial service (see Dispatch FinSa/FinIA, pages 8922, 9010 and 9050).

Unfortunately, the Federal Counsel did not further specify under which of the activities mentioned under Art. 3 let. c FinSA such fund distribution would fall, leading to discussions on whether the distribution of funds will no longer be regulated, i.e., not be covered at all by the conduct rules and the obligation to register as a client advisor under the FinSA. Against this background, the draft FinSO and the first draft of the Explanatory Report clarified from the outset that the term of a “purchase” or “sale” of financial instruments pursuant to Article 3 let. c ciph. 1 FinSA goes beyond circumstances in which there is an effective purchase or sale of a financial instrument. It further made clear that this concept also includes any activity in relation thereto, such as any other action which specifically aims at the purchase or sale of a financial instruments. Such a definition also covers circumstances in which no advice is given to the client, whether transaction-based or in a general form (see Art. 3 para 1 FinSO and Draft Explanatory Report, page 18).

In the first draft of the Explanatory Report, the FDF had stated that the new rules would include any act of “intermediation”. Since the meaning of the term “intermediation” used in the draft version of Article 3 para. 1 FinSO (todays’ para 2) was not precise enough, it has been removed in the final version of Article 3 para 2 FinSO. This article and the Explanatory Report now clarify that “the acquisition or disposal of financial instruments within the meaning of Article 3 letter c ciph. 1 FinSA is deemed to cover any activity addressed directly to certain clients that is specifically aimed at the acquisition or disposal of a financial instrument”. In practice, this will include interactions of financial services providers with specific clients which, based on an assessment of the circumstances, must be considered, potentially or actually, as an important element, or “cause”, to take a specific investment decision.

It seems therefore clear that a contact with an “end investor” is an essential prerequisite for an activity to be characterized as a financial service in the sense of Art. 3 para. 2 FinSO. Against this background, it is very helpful that the Explanatory Report now specifies that the provision of information on financial instruments to supervised financial intermediaries is generally not regarded as a financial service within the meaning of this provision (see Explanatory Report, p. 19). This would only be the case if a financial intermediary exceptionally acquired a financial instrument for its own account (i.e., nostro). This differentiated approach corresponds to the current legal situation (Art. 3 para. 1 CISA) and has proven its merits, as it takes into account the need for protection of end customers without, at the same time, unnecessarily complicating the access of Swiss financial intermediaries to financial instruments, implying the risk of reducing the market for financial instruments in Switzerland, which was clearly not the intent of the legislator. In these cases, the financial services mainly triggering the rules of conduct, take place downstream between the financial intermediary and its clients (see the Explanatory Report, which refers explicitly on page 19 to the required prudential supervision of the respective financial intermediaries).

Whether roadshows should be considered as financial services depends on the specific circumstances of each case. In light of the fact that an activity is only deemed to constitute a financial service in the sense of Article 3 para. 2 FinSO if a certain potential end-investor is addressed directly, specifically aiming at the acquisition or disposal of a specific financial instrument by such client, roadshows will, in many cases, not be characterized as a financial service. However, roadshows will, in other cases, constitute an offer or at least an advertisement for a financial instrument. A roadshow would only constitute the provision of a financial service if, at such an event, specific potential end-investors are additionally approached for the acquisition of a specific financial instrument (for further details see section b) let. i)). In some cases, there might be a thin line between activities constituting only an offer and those which may also be characterized as a financial service. With the new financial market architecture however, those are two independent concepts. Against this background, the general reference to roadshows in the Explanatory Report (see p. 18 seq.) appears to be unfortunate.

ii. Consequences

Article 3 para. 2 FinSO now clarifies under which circumstances the distribution of collective investment schemes is deemed to constitute a financial service under FinSA. If a certain activity is deemed to be a financial service, and only then, mainly the following obligations are triggered: (1) client segmentation (Art. 4 et. seq. FinSA), (2) conduct rules (Arts. 7-19 FinSA), (3) organizational rules (Arts. 21-27 FinSA), registration in the register of advisers (Arts. 28-34 FinSA) and (5) affiliation with an Ombudsman (Arts. 74-86 FinSA).

If financial services are only targeted at professional clients, including institutional clients, according to Article 4 seq. FinSA, certain exemptions to the conduct rules mentioned above and the requirement to register in the registry of advisors may apply:

– According to Article 20 para. 1 FinSA, the provisions of Articles 7-19 FinSA (conduct rules) do not apply to transactions involving institutional clients.

– According to para. 2 of the same article, professional clients may expressly release financial service providers from applying the code of conduct obligations set out under Articles 8, 9, 15 and 16 FinSA.

– Furthermore, financial services providers may assume that professional clients have the necessary knowledge and expertise as well as the capability to assume the financial risks of a specific financial instrument or service (Art. 13 para 2 FinSA).

– With the new Article 31 FinSO, client advisers of foreign financial service providers, which are prudentially supervised abroad, are exempted from the duty to register in the new registry, if the services they provide in Switzerland are exclusively aimed at professional clients, including institutional clients. It is interesting to note however, that this exemption generally does not apply to client advisers of Swiss based companies of the same group.

b) Delimitations

i. Offer vs. financial service

From today’s CISA-perspective, all activities which would constitute a financial service, an offer or advertisement should, in many cases, be considered as distribution according to Article 3 of the existing CISA. However, with the new financial market law architecture entering into force on 1 January 2020 the notions of the financial service, the offer as well as the advertisement for financial instruments and services are three independent concepts. In order to understand how the distribution of funds will be regulated in the future, the difference between these concepts is of fundamental importance.

The term of the offer is defined in Article 3 let. g FinSA as “any invitation to acquire a financial instrument that contains sufficient information on the terms of the offer and the financial instrument itself”. As this definition is not self-explanatory, Article 3 para. 5 and 6 FinSO specify the offer in more detail in both a positive (para. 5) and negative (para. 6) manner.

First, paragraph 5 clarifies that an offer requires a communication of any kind containing (a) “sufficient information on the terms of the offer and the financial instrument” and which (b) “is customarily intended to draw attention to a certain financial instrument and to sell it”. According to the Explanatory Report, this definition in FinSA relies essentially on the definition of the offer under the Swiss Code of Obligations (CO) (see Explanatory Report, p. 20). However, the statement in the Explanatory Report pursuant to which the concept of the offer according to the CO must not simply be understood to apply in any instance where the new legislation refers in general terms to the terms “offer” or “offered”, e.g. in the context of the offering of structured products (Art. 70 para. 1 FIDLEG) or in the context of the approval requirement for foreign collective investment schemes according to Art. 120 CISA, is rather unclear (see Explanatory Report, p. 21). It can therefore only be understood as clarifying that there is a difference between an offer and the issuance of financial instruments from a technical point of view, which would be clear even without this statement. In any case, we are of the view that only a uniform application of the concept of an “offer”, wherever the new legislation triggers legal consequences as a result of the existence of an offer, may achieve the required legal certainty and uniformity in the application of the new legislation.

Finally, paragraph 6 of Article 3 FinSO enumerates constellations which do not constitute an offer. Besides the clarification with respect to making factual information available and the mentioning by name of certain financial instruments, the new specification in the FinSO pursuant to which the fact of making information available at a specific request or initiative of the client without prior advertisement, does not constitute an offer, is the most important clarification in our view. This amendment to FinSO is based on requests from the Fund and Asset Management industry during the consultation process (see amongst others SFAMA’s response in the consultation process). It takes up the current legal situation in Article 3 para. 2 let. a CISA regarding the product-related “reverse solicitation”. This “reverse solicitation” in the specific context of an “offer” must be clearly distinguished from the new regulations on the reverse solicitation in the context of financial services, which are laid down in Art. 2 FinSO and are strictly limited to cross-border circumstances. However, there are good reasons to argue that making information available at the sole request or initiative of the client, without an additional interaction conducted by the service provider, does not constitute a financial service according to Article 3 let. a ciph. 1 FinSO as it must not be considered as the “cause” to take a specific investment decision (see above section 2)let. a)let. i). This would also be in line with the mentioned provision in Article 3 para. 2 let. a of the existing CISA.

Unlike the term of financial service, which triggers the point of sale related obligations, such as conduct and organizational rules and the requirement for registration in the register for advisers, the characterization as an offer is mainly relevant, on the one hand, for the requirement to publish a prospectus and a KID and, on the other hand, with respect to fund specific obligations. Most importantly, a foreign collective investment scheme only needs FINMA approval if it is offered to non-qualified investors according to CISA. The same applies essentially with respect to the appointment of a representative and a paying agent when a product is to be offered to investors other than “per se” qualified investors. Hence, from a fund perspective, the notion of the offer is primarily relevant with respect to non-qualified investors under the CISA. With respect to qualified investors, the qualification as an offer triggers hardly any consequences.

ii. Advertisement vs. financial service

Article 95 FinSO clarifies that any communication which is aimed at investors and serves to draw attention to specific financial services or financial instruments is deemed to constitute advertising within the meaning of Article 68 FinSA. It further outlines circumstances in para. 2 which do not constitute advertisement, such as the mentioning by name of financial instruments, the provision or forwarding of communications from issuers and reports in the trade press. This indicates that the scope of application of the term advertisement according to the FinSA is narrower than under the existing CISA-regime.

Similar to the offer as described above, advertisement hardly trigger any requirement for “per se” qualified investors according to the CISA. Unlike for other financial instruments, where no product specific approval requirement exists, an advertisement triggers the product specific approval requirements, as well as the obligation to appoint a representative and a paying agent, according to Article 120 para. 1 and 4 CISA. A corresponding specification in a new Article 127a CISO has been added in the final version of the updated CISO to ensure that the special statutory obligations of the CISA will not be undermined by the FinSA as a result of an advertisement to non-eligible target investors. This is also in line with the remaining provisions of CISA and CISO, such as, in particular, Art. 133 para. 2 CISO. By contrast, in respect of financial instruments other than collective investment schemes, the initially proposed Article 95 para. 3 of the draft version of FinSO has now been suppressed from the final version of the

ordinance. The fact that some of the original commentary of this norm in the draft Explanatory Report can still be found in the final version of this report could, however, lead to some uncertainty with respect to other financial instruments.

3) Transitional provisions

An important part of the final version of the FinSA from a CISA perspective are the transitional provisions, particularly Articles 105 and 106 FinSO. On 1 January 2020, the new regulatory regime enters into force. Consequently, many provisions of the CISA, including the definition of the concept of “distribution” and “non-distribution” (Art. 3 CISA), as well as the conduct and organizational rules at the point of sale (Art. 20 et seqq. CISA), will cease to exist. The requirement to obtain a distributor’s license and to conclude a distributor’s agreement will also disappear. However, with the transitional provisions provided for in Article 103 et seqq. FinSO, the effective date of practically all new FinSA requirements, in particular the conduct and organizational rules, will be pushed back until 1 January 2022. As for the obligations to register with the registry for advisors and to be affiliated with an Ombudsman, there is a transitional period of six month from the moment the registry, or the Ombudsman, have been approved by FINMA or the FDF, respectively.

As the existing CISA rules at the point of sale will cease to exist by the end of this year, but the effective date of the new equivalent rules of FinSA will be pushed back for another two years, there is a time gap with respect to the conduct and organizational rules at the point of sale and a risk of legal insecurity. Against this background, the transitional provisions of the final version of FinSO provide for a phasing out of some of the current CISA rules over the course of two year. It is interesting to note that those transitional provisions also apply to financial services providers entering the Swiss market after 1 January 2020 (See Explanatory Report, p. 68), which, in our view, seems very unusual.

With Article 105 and 106 para. 3 FinSO, financial service providers are subject to the existing rules of conduct and organizational provisions according to Article 20 – 24 CISA (as per 31 December 2019), until they comply with the new provisions of FinSA. This includes not only compliance with CISA and its implementing ordinance CISO, but also with the relevant SFAMA self-regulations. Consequently, this also means that the existing regulatory requirement to conclude distribution agreements remains in place. This further explains why the current requirement for foreign collective investment schemes to appoint a representative and a paying agent irrespective of whether the funds are distributed to qualified or non-qualified investors continues to apply until a financial service provider fully complies with FinSA. Without these requirements, the current concept of distribution agreements, the representative being a party of such agreements, would not work.

It is to the discretion of each financial service provider to decide when they will comply with the new FinSA regulation. However, according to para. 2 of Article 105 and 106 FinSA, financial services providers implementing the new rules before the end of the transitional period must inform their audit firm. This creates clarity as to which supervisory regime applies to the respective financial service provider (see Explanatory Report, p. 69). Against this background it seems clear to us that this reporting obligation can only apply for financial service providers required to undergo prudential audits in Switzerland either based on prudential supervision or a distribution agreement in the sense of Article 24 para. 2 CISA (as per 31.12.2019) in conjunction with Article 105 and 106 para. 3 let. d FinSO. From a practical point of view, to terminate the distribution agreement required by the current version of CISA once a financial service provider complies with FinSA, a formal notice to the parties of the distribution agreement, e.g. the representative for foreign funds, is in our view further required.

Even though existing CISA rules on conduct and organization at the point of sale will remain in place until a specific financial service provider decides to comply with the new FinSA rules, all remaining changes of the CISA, such as the abolition of the term distribution, will be effective on 1 January 2020. This can lead to peculiar situations in which an existing regulation based on the term distribution remains applicable, but adapted to the new concept of a “financial service”. In particular at the intersection between the new law and the existing CISA provision, such as client segmentation, special caution with regard to necessary measures to be implemented by the end of 2019 is required. However, even though this approach appears to be somewhat unconventional, from the perspective of the investors’ protection, but also from the perspective of the industry, it should be the least disruptive given the decision of the legislator to favor an ongoing continuous implementation of the new financial market architecture as regards the FinSA rules of conduct and organization over a relative long period of two years.

4) Conclusion

The FinSA and the FinIA will, with their entry into effect on 1 January 2020, materially change the existing financial regulatory concepts in Switzerland, in particular in the context of the distribution and management of collective investment schemes. This being said, it is to be noted that the interaction of the new concepts of a financial service, an offer of and advertisement for financial instruments or services leads in practice to more flexibility as compared to the existing single test under Article 3 CISA of a “distribution” of collective investment schemes. This will allow financial promotors to implement in their placement activities a differentiated approach, in particular in circumstances which today constitute a distribution and where contacts with end-investors are subject to the stringent and inflexible regulations under Article 3 CISA.

With the new financial market law architecture, only when a certain activity is deemed to constitute a financial service, and only then, the new FinSA obligations at the point of sale, such as conduct and organizational rules or the requirement to register in the new register for advisors, are applicable. As the existing CISA rules at the point of sale will cease to exist by the end of this year, but as the effective date of the new equivalent rules under FinSA will as a matter of facts be pushed back for another two years, transitional provisions have been added to the final version of the ordinance. Generally speaking existing CISA rules on conduct and organization will continue to exist until a financial service provider fully complies with the new FinSA. This will lead to an implementation phase where, as a matter of fact, there will be a number of gray zones and uncertainties. This seems however to be accepted by the legislator, in particular at the intersection between the new law and the existing CISA provision, such as for the purpose of implementing the new client segmentation. In this respect, a special attention needs to be paid to the necessary operational measures which are required for a timely implementation of the categorization of existing non-qualified investors, who as a matter of law will be characterized with the entry into effect of FinSA as qualified investors.

All in all, these fundamental legislative changes in Switzerland will bring a welcome additional flexibility, in particular with a view of enhancing the competitiveness of Switzerland as a financial market place, mainly where institutional or professional investors are contacted. This holds in particular true for the cross-border offer of financial instruments or services as a result of the conscious choice of the legislator to waive the registration requirement for prudentially supervised foreign financial services providers. This must be seen as a clear sign of openness of Switzerland towards other jurisdictions.

The content of this article is the personal opinion of the authors. This opinion is not necessarily identical with the position of Lenz & Staehelin or SFAMA.

Diana Imbach Haumüller (diana.imbach@sfama.ch)

François Rayroux (françois.rayroux@lenzstaehelin.com)