Reporting of Beneficial Ownership in Unlisted Companies according to Article 697j CO – Some Open Points

On July 1, 2015, new rules regarding reporting of beneficial owners of unlisted companies entered into force in Switzerland (for general remarks on the rules see CapLaw-2015-55). Even four years after their implementation, there are still a number of open questions in practice as regards the application of these rules, both from the perspective of the shareholders (subject to the obligation to report their beneficial owners(s)) and the companies (subject to the obligation to maintain a register of beneficial owners). One reason for these uncertainties is that the relevant provisions are incomplete and in many aspects leave room for interpretation. To date there is no case law that could provide guidance. A currently ongoing revision of the disclosure rules could bring some clarity.

By Alexander Wille / Lukas Held (Reference: CapLaw-2019-16)

1) Legal Basis

According to article 697j (1) Code of Obligations (CO), any person who alone or in concert with third parties acquires shares in a company whose shares are not listed on a stock exchange, and thus reaches or exceeds the threshold of 25% of the share capital or voting rights, must within one month give notice to the company of the name and the address of the natural person for whom it is ultimately acting (the beneficial owner). The notification obligation applies to the acquisition of bearer shares (Inhaberaktien) and registered shares (Namenaktien). Non-compliance with this provision has severe consequences: The membership rights (in particular voting rights) are suspended for as long as the shareholder has not made the required notification (article 697m (1) CO). Financial rights (in particular right to receive dividends) may only be exercised once disclosure has been made and are forfeited for the period until disclosure is made (article 697m (2) and (3) CO). Companies must keep a register of the beneficial owners reported by shareholders to the company (article 697l CO).

The Act on the Implementation of the Recommendations of the Global Forum on Transparency and Exchange of Information for Tax Purposes (Global Forum Act) is currently being discussed in the Swiss Parliament. The Global Forum Act also provides for amendments of the provisions on disclosure of beneficial owners. The intention behind the proposed amendments is to eliminate some of the ambiguities raised during the consultation process regarding the application and interpretation of article 697j CO. It is envisaged that the Global Forum Act will come into force on October 1, 2019.

The obligation of shareholders to report their beneficial owner(s) and the obligation of companies to maintain a register of beneficial owners are equally applicable to companies limited by shares (Aktiengesellschaften; AG) and to limited liability companies (Gesellschaften mit beschränkter Haftung, GmbH). For the sake of simplicity, in this article reference is solely made to the provisions applicable to companies limited by shares.

This article focuses on some selected practical cases as to which the application of article 697j CO has raised questions. For a general overview reference is made to the legal literature on the topic.

2) Private Equity Funds

a) General Remarks; Beneficial Owner

The record-high deal activity in the private equity sector in recent years led to the acquisition of many private Swiss companies by private equity funds.

The application of the disclosure provision of article 697j CO caused uncertainties in the context of acquisitions by private equity funds. The key question is whether there is at all a beneficial owner within the meaning of article 697j CO in a private equity fund to be reported to the portfolio company (the beneficial owner is defined in 697j CO as “natural person for whom it [the acquirer] is ultimately acting” (“Personen (…) für die er [der Erwerber] letztendlich handelt”)). To determine whether there is a beneficial owner within the meaning of article 697j CO requires a closer look on the ownership and control structure of a typical private equity fund.

b) Typical Private Equity Fund Structure: Impact on Beneficial Ownership

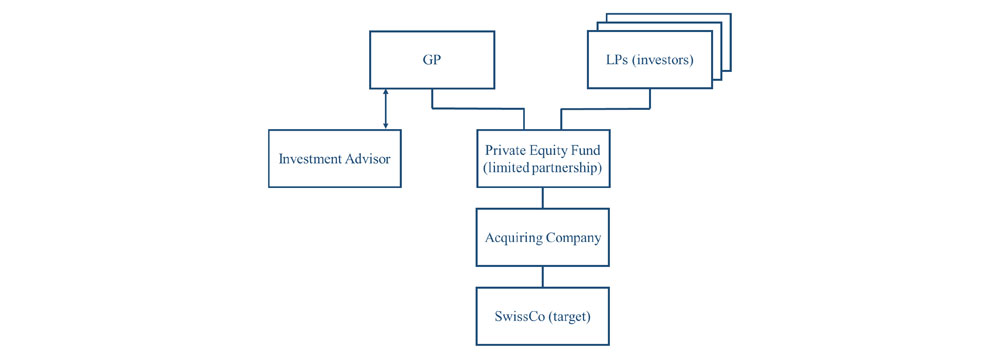

The typical private equity structure (which is the basis for the subsequent remarks) is as follows: At the top of the structure is a private equity fund structured in the form of a limited partnership. The investors of the fund are the limited partners (LPs) of the partnership and the administration and management of the fund is in the hands of the general partner (GP). The GP often delegates management and investment decisions of the fund to an investment advisor controlled by the partners of the private equity fund. Despite this delegation, the GP remains ultimately responsible for investments of the fund and has the power to act on behalf of the fund. A private equity fund typically invests in portfolio companies through one or several acquisition vehicles controlled by the fund. Below is a simplified overview of a typical private equity structure:

While the GP is responsible for the investment decisions and exercises control rights in the portfolio company, the GP does not economically benefit from the performance of the portfolio company (at least not directly). The investors, on the other hand, are contributors of capital and participate in the performance of the portfolio companies. However, investors typically do not have any say on the management of the fund, the investment of the funds’ assets and the exercise of control rights in the portfolio company. In most cases, investors hold small positions in private equity funds which do not allow them to influence the GP in its management and investment decisions.

Economic ownership rights and control rights over the portfolio company typically fall apart in a private equity structure. According to the predominant view in legal doctrine, neither the GP nor the investors qualify as beneficial owners within the meaning of article 697j CO.

c) Exception: Controlling Investor(s)

Exceptionally, an investor is considered as beneficial owner, if it has a controlling influence on the private equity fund and, thus, might indirectly exercise control in the portfolio company. The same applies if not an individual investor but several investors acting in concert have a controlling influence over the private equity fund. According to a view in legal doctrine an investor should be considered as having controlling influence if it indirectly holds an interest of 25% or more in the acquired company (the 25% threshold is in line with the definition of beneficial owner in article 2a Anti-Money Laundering Act (AMLA)). Control of an investor may also be based on the specific contractual set up for the private equity fund.

d) Reporting of Beneficial Owners

Beneficial owners must be reported to the company within one month after an acquisition of 25% or more of the share capital or voting rights (article 697j (1) CO). Neither law nor legislative materials provide for provisions regarding the form in which the notification of beneficial owners has to be made. For evidentiary purposes, the notification should be made in written form.

As set out above, in a typical private equity set up there should be no beneficial owner within the meaning of article 697j CO to be reported to the portfolio company. However, this view has so far not been tested and a court might come to a different conclusion as to beneficial ownership in a private equity fund. Given these legal uncertainties and the severe consequences in case of non-compliance with the reporting obligation in article 697j CO, it is advisable that a private equity fund (through its acquisition vehicle) nonetheless makes a notification to the portfolio company (sometimes referred to as negative notification (Negativmeldung)).

In such notification, it is stated that there is no beneficial owner within the meaning of article 697j CO (unless there is a controlling investor (or several controlling investors acting in concert), in which case such investor(s) would be reported as beneficial owner(s)). To provide transparency as regards ownership and control, the notification may include a description of the organizational structure from the direct shareholder up to the private equity fund. On the level of the private equity fund, it may be confirmed that there is no investor (or several investors acting in concert) with controlling influence on the private equity fund (e.g., by disclosing that there is no investor with an interest in the fund above a certain percentage threshold). The notification may also disclose the name of the highest-ranking manager of the GP, since this person may be considered as having significant controlling influence over the portfolio company

(however, this information may be of limited value as over the course of time the highest-ranking manager may change).

e) Register of Beneficial Owners

According to article 697l CO, companies are required to keep a register of the beneficial owners reported to the company. The company (acting by its board of directors) has generally no obligation to verify the notifications of beneficial owners received from its shareholders and has no right to deviate from such notifications when maintaining the register of beneficial owners (e.g. by including beneficial owners in the register not reported by shareholders).

If a company receives a negative notification (i.e., no person(s) reported as beneficial owner(s)) from the acquiring company of the private equity fund, it should reflect such negative notification in its register of beneficial owners. In our view, this may be done by adding a remark in the register that no beneficial owner within the meaning of article 697j CO exists and by making a reference to the notification received from the shareholder.

The notification (and any additional documents provided by the reporting shareholder) must be retained by the company for ten years following the deletion of the reporting shareholder from the company’s share register (article 697l (3) CO). To ensure that notifications are not lost, they should be kept with, or attached to, the register of beneficial owners.

f) Revision under Global Forum Act

According to the current draft of the Global Forum Act, the existing article 697j CO is to be extended by a new article 697j (2), which should clarify the concept of beneficial ownership. If the direct shareholder is a legal entity or a partnership, the natural person who controls the shareholder in the meaning of article 963 (2) CO must be reported as beneficial owner (article 697j (2) draft CO). If there is no such person, the Global Forum Act clarifies that the shareholder must notify the company accordingly (negative notification).

In analogous application of article 963 (2) CO, the beneficial owner is the natural person who (a) directly or indirectly holds the majority of the voting rights in the direct shareholder, (b) directly or indirectly has the right to appoint or remove the majority of the members of the board of directors of the direct shareholder, or (c) can exercise a controlling influence over the direct shareholder by virtue of the articles of association, the foundation deed, a contract or comparable instruments. These criteria to determine the beneficial owner are based on exercising control over the shareholder.

In our view, for acquisitions by private equity funds the proposed change to article 697j CO means that in the future the individual(s) ultimately controlling the GP would qualify as beneficial owner(s), since the GP exercises control rights over the direct shareholder of the portfolio company. Hence, other than under current law, a beneficial owner in the sense of article 697j CO would also exist in typical private equity structures. As stated above, if there is/are no individual(s) controlling the GP, this fact must be reported to the portfolio company. It may be appropriate to include the name and address of the highest-ranking manager of the GP (e.g., CEO, chairman of the board) in such negative notification. If in exceptional circumstances there is a controlling investor (or several controlling investors acting in concert), such investor(s) has/have to be disclosed as beneficial owner(s). Depending on the specific form of control, the controlling investor(s) would have to be reported as beneficial owners alone or together with the individual(s) controlling the GP.

3) Listed Companies

a) General Remarks; Partial Listing

The reporting obligation of article 697j CO only applies to companies whose shares are not listed on a stock exchange. The provision does not apply to the acquisition of shares in listed companies. Reason for the exemption for listed companies is that disclosure rules applicable to listed companies (e.g. article 663c CO and article 120 Financial Market Infrastructure Act (FMIA)) ensure sufficient transparency on beneficial owners.

According to predominate view in legal doctrine, the exemption from the reporting obligation of article 697j CO also applies if the acquired shares are not listed, but other equity securities (Beteiligungsrechte) of the company are listed on a stock exchange (e.g., listed bearer shares and non-listed registered shares or vice versa). Sufficient transparency is ensured in such circumstances, because the notification obligation under article 120 FMIA is applicable and also extends to non-listed shares.

b) Listed Shareholder or Listed Parent Company of Shareholder

The wording of article 697j (1) CO implies that the exemption from the reporting obligation only applies if the acquired company itself is listed on a stock exchange and that the reporting obligation would apply if a listed company (directly or indirectly through a subsidiary) acquires shares in an unlisted company.

An obligation to report the beneficial owner in cases where a listed company (directly or indirectly through a subsidiary) acquires a majority interest in an unlisted company would not create any additional transparency. The same persons disclosed as beneficial owners to the listed company under applicable stock exchange law would be reported as beneficial owners to the acquired company. In line with the purpose of article 697j CO, which is to create transparency about the beneficial owners of unlisted companies, an exemption to the reporting obligation seems justified. The exemption also applies to all (direct or indirect) majority-controlled subsidiaries of the listed company. This view also corresponds with the AMLA according to which a financial intermediary does not have to determine the beneficial owner of a company listed on a stock exchange or a company that is majority-controlled by a listed company (see article 4 (2) AMLA).

The reporting obligation of article 697j CO applies if a listed company (directly or indirectly) acquires a minority interest in an unlisted company.

c) Foreign Stock Exchange

Article 697j CO leaves room for interpretation as to whether the exemption from the reporting obligation only applies with respect to companies listed in Switzerland or also with respect to companies listed on a foreign stock exchange (more precisely, the question is whether listed companies that are not subject to article 120 FMIA are exempted from article 697j CO). According to legal doctrine, the exemption from the reporting obligation applies with respect to acquired companies listed on a foreign stock exchange, if the applicable disclosure rules provide for equivalent transparency as under Swiss law. Under the conditions set out in Sec. 3b) above and provided that the applicable disclosure rules provide for equivalent transparency, the exemption also applies if the acquiring company or the parent company of the acquiring company are listed on a foreign stock exchange.

In practice, it is difficult to assess what equivalent transparency means and whether the foreign disclosure regime provides for such equivalent transparency. In our view, equivalent transparency can already be assumed if the applicable stock exchange law provisions ensure a disclosure standard which aims to effectively identify significant shareholders and their beneficial owners, even if the individual provisions are less far-reaching than Swiss stock exchange law (e.g. first threshold higher than 3% as provided for under article 120 FMIA). Transparency would not be sufficient if, for example, only the shareholder and not the beneficial owner(s) of such shareholder had to be disclosed under the relevant provisions. It should also be verified whether in case of a partial listing, disclosure under the respective foreign stock exchange law also extends to the non-listed shares (see Sec. 3a)).

d) Reporting of Beneficial Owners

The acquisition of 25% or more of the share capital or the voting rights in a listed company does not trigger a reporting obligation pursuant to article 697j CO.

As set out in Sec. 3b) above, the (direct or indirect) acquisition of a controlling interest in an unlisted company by a listed company should be exempted from the reporting obligation. However, due to legal uncertainties associated with such interpretation of article 697j CO, a notification should be made to the company, in which it is disclosed that the shares of the acquirer (or the parent company of the acquirer, as the case may be) are listed on a stock exchange. The notification may include information providing additional transparency on the listed company and the applicable disclosure regime, such as the following: stock exchange where the shares of the company are listed, lowest threshold triggering a disclosure obligation under applicable stock exchange laws, list of shareholders exceeding lowest notification threshold at the time of the notification and reference to where updated disclosure notifications and a list of important shareholders may be found (e.g. link to the relevant website of SIX or the listed company). Besides that, it is not necessary to state the beneficial owner(s) of the listed company. Such a notification should also be made in case of an acquisition of a minority interest in an unlisted company by a listed company.

If the company is listed on a foreign stock exchange and the applicable disclosure rules are deemed not to be equivalent to the Swiss disclosure rules, the beneficial owner(s) of the listed company will have to be disclosed to the acquired company.

e) Register of Beneficial Owners

The register of beneficial owners of the company receiving a notification will reflect the fact that the shares of the shareholder (or its parent company as the case may be) are listed on a stock exchange. Additional information regarding the listed company and its ownership disclosed in the notification (see Sec. 3d)) may be summarized in the register of beneficial owners. Alternatively, a reference to the notification is made in the register of beneficial owners.

f) Revision under Global Forum Act

The revision clarifies that an exemption to the reporting obligation applies if only part of the equity securities of a company are listed on a stock exchange, even if the acquired shares are not listed (article 697j (1) draft CO; replacement of the wording “shares” (Aktien) by “equity securities” (Beteiligungsrechte)).

In addition, the revision of article 697j CO intends to eliminate the ambiguities with regard to acquisitions by listed companies (or by companies controlled by listed companies). Under the proposed changes, a shareholder whose equity securities are listed on a stock exchange and a shareholder who is controlled by a listed company within the meaning of article 963 (2) CO or who controls such a company must only report this fact and the name and registered office of the listed company (article 697j (3) draft CO).

The dispatch on the Global Forum Act states that this also applies to a listing abroad, provided that equivalent transparency is guaranteed. Since the dispatch does not further elaborate on this, the difficulties connected with the assessment of equivalence (see Sec. 3c)) remain even after the revision of the law.

4) Change of Beneficial Owner without Transfer of an Unlisted

Companies’ Shares

Pursuant to article 697j (2) CO, any shareholder who had to report its beneficial owner(s) has to report any change in the name or the address of the beneficial owner to the company. The law does not provide for a term for the fulfilment or for legal consequences in the event of non-compliance with this obligation. In our opinion, due to the lack of a specified term, a breach of this obligation has no consequences.

The scope of said provision is rather unclear. What is clear is that the changes specified in article 697j (2) CO (i.e., changes to the first name, last name or the address of the beneficial owner) must be reported to the company. Further, in accordance with prevailing legal doctrine, it can be assumed that other changes at the level of the beneficial owner (e.g. change of the level of shareholding) do not have to be reported to the company.

In practice, the situation in which the beneficial owner changes without a transfer of shares in the unlisted company causes difficulties. For illustrative purposes, we assume a beneficial owner (BO) who sells to a third party all shares in a wholly owned subsidiary (SubCo), which in turn holds 25% or more of the share capital or voting rights of an unlisted Swiss company (SwissCo). As mentioned above, in such case only the BO changes but not SubCo as direct shareholder entered in the share register of SwissCo. According to the wording of article 697j (1) CO, there is no reporting obligation in this case due to the lack of an acquisition of shares in SwissCo.

It is questionable whether in such cases there is a reporting obligation regarding the change of the BO based on article 697j (2) CO. The provision refers to a “change in the first or last name or address of the beneficial owner” (“Änderung des Vor- oder Nachnamens oder der Adresse der wirtschaftlich berechtigten Person”). Such a change also occurs in our initial case. With a view to the relevant dispatch, however, it can be assumed that the legislator did not want to introduce an additional reporting obligation in article 697j (2) (besides article 697j (1)) (note though, that recent views in legal doctrine take the view that such a reporting obligation exists).

Even if this view would be preferable in order to ensure the envisaged transparency, in our view no reporting obligation arises de lege lata in our initial case where only the BO changes but no transfer of shares of the SwissCo occurs. Article 697j (2) only deals with the change in the personal details of the BO already reported pursuant to article 697j (1). This conclusion is also supported by the practical problem that SubCo may not know and may not have the means to ensure timely knowledge of all changes of its beneficial owner(s).

5) Maintaining the Register of Beneficial Owners

As counterpart to the reporting obligation of shareholders, companies a required to maintain a register of beneficial owners (article 697l CO). The law does not make any specifications as to the form of such register. The register may be combined with the share register (e.g., by adding additional columns to the share register) or kept as a separate register (e.g., by annexing the register of beneficial owner to the share register). The register of beneficial owners has to contain first name, last name and address of the individuals reported to the company as beneficial owners (article 697l (2) CO). According to the wording of the law, the company is obliged to keep the register of the beneficial owners reported to the company. Within a company, this obligation is in principle imposed on the board of directors.

It is unclear when the obligation for companies to first “create” a register of beneficial owners is triggered. The questions arises, because holders of registered shares are not required to report their beneficial owner(s) if they held 25% or more of the share capital or the voting rights of a company already prior to the entry into force of the disclosure provisions on July 1, 2015. Consequently, many companies with registered shares have to date not received any notifications from their shareholders because no transfers in their shares triggering the notification obligation have occurred since then. Article 697l CO does not exempt companies from maintaining a register in such circumstances. However, in our view the wording “of the beneficial owners notified to the company” (“die der Gesellschaft gemeldeten wirtschaftlich berechtigten Personen”) in article 697l (1) CO indicates that the obligation is only triggered upon receipt of a (first) notification of beneficial owners. It does not create any transparency if prior to the first notification, companies maintain an empty register of beneficial owners. This problem should not arise with regard to companies with bearer shares, since holders of bearer shares had to notify their beneficial owners to the company within one month after coming into force of the provisions on July 1, 2015 and the company then entered such beneficial owner in the register.

Alexander Wille (alexander.wille@lenzstaehelin.com)

Lukas Held (lukas.held@lenzstaehelin.com)