Proposed Regulatory Framework for Financial Products in Switzerland

Two new pillars of financial markets regulation are currently being elaborated in Switzerland. The proposed laws will have a strong impact on banks, securities dealers, issuers and distributors of financial products, fund management companies, external asset managers, individual client advisors, and trading venues with respect to the legal structuring, distribution, trading, and clearing and settlement of financial products. This article provides a brief overview on the expected key points of the new laws and sets out their potential effects on financial product providers in Switzerland.

By Luca Bianchi (Reference: CapLaw-2014-5)

1) Introduction

The collapse of Lehman Brothers on 15 September 2008 and the following financial crisis (including the Madoff Scandal) have led to various global regulatory changes. In this context, the legislation in the European Union (EU) has (and continues to have) a strong impact on Swiss regulatory developments. Consequently, the changes that are in the process of being introduced in the EU by the Markets in Financial Instruments Directive (MIFID II) and the European Market Infrastructure Regulation (EMIR) are similarly being implemented in Switzerland through two new pillars of financial markets regulation. The proposed Financial Services Act (FFSA) is expected to regulate the creation of financial products and related services (including distribution). Furthermore, the proposed Financial Market Infrastructure Act (FMIA) is expected to contain rules on trading venues, OTC-derivatives clearing and settlement, and the general transparency of derivative markets. Both laws aim to install consistent rules (i.e. a level playing field) for all financial product providers and other market participants.

2) Financial Services Act (FFSA)

a) Scope of the new Law

The new law targets a cross-sector regulation of financial products and services, mandates extended investor protection at the point of sale, and enhances the supervision of certain market participants (cp. Federal Department of Finance (FDF), Financial Services Act (FFSA) − Key thrusts of potential regulation, 18 February 2013, 1 et seq.).

b) Key Points

The FFSA is expected to cover the following key points:

i) Prospectus duty for all securities

All securities offerings that are issued in or from Switzerland will be subject to the duty to publish a prospectus. The new law will likely provide for exceptions in connection with securities offerings with a minimum denomination of CHF 100,000 which are addressed to a restricted circle of investors and certain other specifi c situations. The structuring and content of the prospectus will also be regulated. In addition, a legal basis for a cross-product prospectus liability may be implemented to the new law.

ii) Key Investor Information Document (KIID)

For all complex financial products a KIID must be published and offered to retail clients free of charge before the subscription/purchase of the product. Complex financial products will presumably comprise standard or tailor-made combined products that consist of different parts (i.e. structured products, fund shares/units, certain insurance investment products, and bonds with particularly complex features). The KIID will be required to contain a simplifi ed product description and risk disclosure to facilitate the comparison and understanding of different products for retail investors.

iii) Duties at the point of sale

Regulated and unregulated financial service providers will be subject to a cross-sector code of conduct containing minimum requirements applicable for all market participants. In particular, distributors of financial products may be obliged to perform suitability checks and fulfi ll documentation and information duties regarding characteristics, costs (including a disclosure of third-parties remunerations) and risks of financial products.

iv) Client segmentation

Market participants will be required to inform clients as to which client segment they are allocated (qualifi ed investors vs. non-qualifi ed investors). Under certain circumstances, non-qualifi ed investors will have the possibility to opt-in to the qualifi ed investor status based on their know-how, professional experience, and/or a minimum wealth requirement in order to benefi t from a more sophisticated investment universe. On the other hand, some qualifi ed investors will likely have the option to opt-out of the qualified investor status in order to benefi t from investor protection.

v) Regulation of external asset managers

External asset managers will potentially be subject to more intense rules of conduct and prudential supervision by either FINMA or self regulatory organizations (i.e. SROs).

vi) Licensing requirements for individual client advisors

Individual client advisors which perform the distribution of financial products will most likely need to publicly register as licensed client advisors. The existing licensing requirements for institutions acting as distributors of collective investment schemes will, potentially, be abolished and replaced by the licensing requirements for individual client advisors.

vii) Regulation of cross-border activities into Switzerland

It is expected that foreign financial services providers will have to comply with the same code of conduct as Swiss providers for their cross-border activities (including the requirement to perform suitability checks). Thus, they will have to inform their Swiss-based clients (and their clients that are covered from Switzerland) about themselves, their services, and their products. Furthermore, foreign financial services providers will either have to register or, conceivably, establish a branch in Switzerland. However, it is possible that equivalent home country rules will be suffi cient in certain cases. The above key points are based on current expectations and may be subject to amendments during the legislative process.

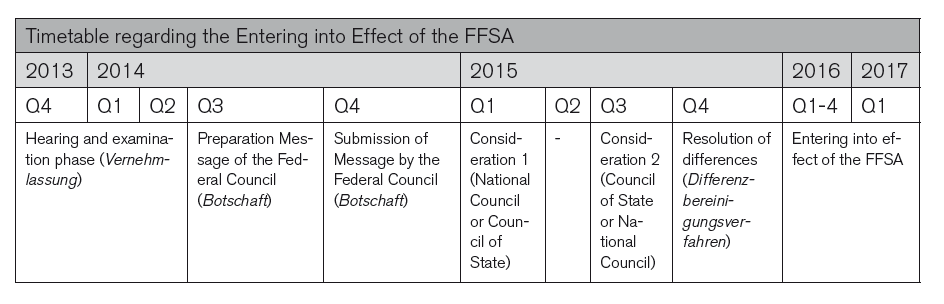

c) The Road to FFSA

The following timetable represents an indicative schedule for the implementation of the FFSA. Financial product providers should be aware that the legislative process may differ from the dates set out below.

d) Possible Effects on Financial Product Providers

The FFSA will have a strong impact on financial product providers with respect to the legal structuring of financial products. Primarily, the required documentation for new products will be affected (and potentially more cumbersome). Furthermore, the new law may have an impact on existing product documentation, distribution agreements, internal guidelines, and the setup of the sales process (including the education of the sales force as well as the required registration of all individual client advisors). In conclusion, the new law will have massive consequences for the production and the distribution of financial products.

3) Financial Market Infrastructure Act (FMIA)

a) Scope of the new Law

The purpose of the FMIA is to enhance the functioning, the stability, and the transparency of financial markets as well as the protection and equal treatment of investors (cp. Preliminary Draft of the FMIA (PD-FMIA) and Federal Department of Finance (FDF), Financial Market Infrastructure Act − Preliminary Draft to the Consultation Proposal of 29 November 2013, 1 et. seq.).

b) Key Points

The FMIA will set out rules on the following key aspects:

i) Regulation of trading venues

Licensing duties for stock exchanges, multilateral trading facilities (MTFs) and organized trading facilities (OTFs) that allow, and in some cases restrict, multilateral trading will be implemented. In principle, the same general authorization requirements will apply for all trading venues (in particular, concerning organization standards, proper business conduct requirement, outsourcing, and capital requirements). However, the principle of self-regulation will continue to apply. Non-Swiss trading venues will be obliged to obtain recognition by FINMA before they grant access to Swiss participants that are regulated by FINMA.

ii) Regulation of post-trading infrastructure

Central counterparties, central custodians, transaction registers, and, potentially, payment systems, will be subject to licensing requirements. Respective authorization requirements will be included to the new law. In addition, duties and provisions concerning the handling of insolvencies of systemically relevant post-trading infrastructures will be installed.

iii) Transparency

Trading transparency and market monitoring will be enhanced. In particular, a transaction register will be implemented.

iv) Derivatives Trading

The new law aims for an implementation of clearing, notifi cation, and risk minimizing duties for all derivatives (not only OTC-derivatives). It will include the duty for some counter-parties to settle trades over a central counterparty (CCP). In addition, some counter-parties will be obliged to trade all derivatives on a FINMA-approved or recognized trading platform or venue. FINMA will have to specify which derivatives will be subject to this rule based on the following criteria: standardization, liquidity, trading volume, price transparency, and counterparty risk. Furthermore, counterparties of derivatives transactions will be obliged to notify a FINMA-approved or recognized transaction register with respect to their derivatives transactions.

v) Rules on Market Conduct

The current rules on market conduct will be subject to the new law. The provisions regarding the disclosure of share holdings, public offers, insider trading, and market manipulation will be transferred to the FMIA.

vi) Penal provisions

The criminal sanctions concerning breaches of the professional secrecy, documentation or notifi cation duties, duties related to derivatives trading, disclosure duties, public offer related duties, as well as insider trading, and price manipulation will be inserted to the FMIA. Breaches of these provisions may lead to major penal sanctions. The key points of the law outlined above are based on currently available public information. The actual content of the law may be subject to amendments in the course of the legislative process.

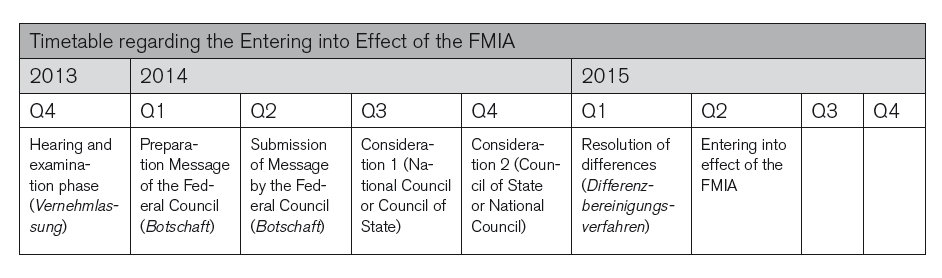

c) The Road to FMIA

The following timetable represents an indicative schedule for the implementation of the FMIA. However, the legislative process may differ from this indicative schedule and readers should be aware that the below stated dates may not be accurate.

d) Possible Effects on Financial Product Providers

The FMIA will affect the clearing and settlement of OTC-derivatives, including structured products, either directly and/or with respect to hedging transactions. In consequence, adjustments to operative processes, updates of related agreements as well as changes in the product documentation will be required. Therefore, all financial product providers should continue to monitor the potential impact of the new legislation on their business models and, eventually, adapt to the new rules. Due to the major penal sanctions regarding breaches of some provisions of the FMIA, compliance with the respective provisions will become very important.

4) Conclusion

The entering into effect of the FFSA and the FMIA will initiate a new era of financial product regulation in Switzerland. Once the drafts of the new laws are published, market participants need to assess whether and to what extent, their business will be affected. Subsequently, market participants targeted by the new laws will need to begin preparations for the necessary adjustments to their business. CapLaw will continue to report on important questions and developments on the road to the FFSA/FMIA.