P.R.I.M.E. Finance – the Boon and Bane of a Specialized Dispute Resolution Institution

P.R.I.M.E. Finance is an arbitral institution specialized in the settlement of financial disputes that was established in The Hague in 2012. As a relatively novel arbitral institution it is not only facing promising opportunities but also difficult challenges.

A hotly debated topic is P.R.I.M.E. Finance’s closed list of arbitrators from which the parties are obliged to choose. While the list includes specialists with expertise in finance and arbitration, it is nevertheless exclusive and may therefore lose attractiveness vis-à-vis other arbitral institutions. Another issue is the publication of awards by P.R.I.M.E. Finance. Even though the transparency of awards helps to build up a consistent body of law aiming at more legal certainty in the financial markets, parties may be unwilling to trade off the confidentiality advantage of arbitration.

Despite these challenges, P.R.I.M.E. Finance may have a positive market resonance. In September 2013, its model arbitration clause has been hardwired into the first Arbitration Guide of the International Swaps and Derivatives Association (ISDA), a market with a tremendous volume.

By Désirée Klingler (Reference: CapLaw-2015-43)

1) Do we need P.R.I.M.E. Finance?

The necessity of P.R.I.M.E. Finance is a central question that founders and critics have addressed likewise. Even though the institution has not decided a case yet, mostly being occupied with the issuance of expert opinions, it may nevertheless play an important role in future dispute settlement.

a) Bridging Gaps between Jurisdictions

Making use of the New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards of 1958 (New York Convention), which applies in over 150 jurisdictions, P.R.I.M.E. Finance may rely on a well-established and relatively simple mechanism for the enforcement of its awards.

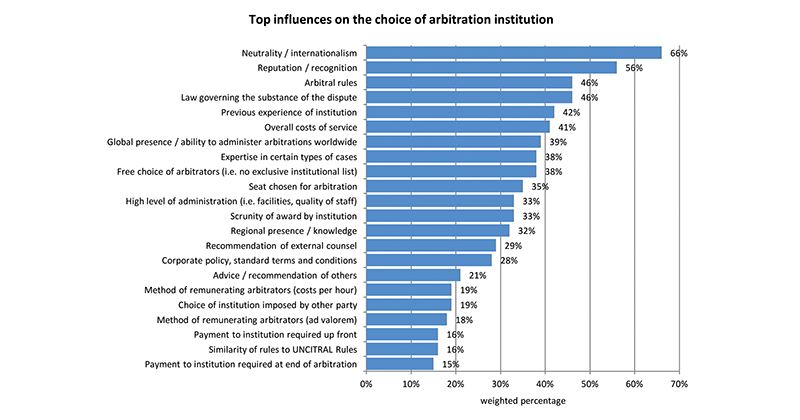

Another advantage is P.R.I.M.E. Finance’s location. The Hague has not only a long-standing history of international judiciary, hosting for example the International Court of Justice, but is also known for its political neutrality. According to the International Arbitration Survey 2010, neutrality is perceived as the most important factor in the choice of an arbitration institution (66%, Graph 1).

Graph 1: International Arbitration Survey 2010

In this respect, The Hague provides for a good compromise to Anglo-American market participants and Asian parties that have become active players in the financial markets in recent years.

b) Trend for Specialized Courts

Over the last decades, a trend for specialized courts may be observed. In Switzerland for example, the Federal Administrative Court with a division specialized in financial market regulation has been established. This trend for specialization may also be observed in the realm of arbitration: Both the ICC Arbitration Court and the London Court of International Arbitration (LCIA) are designed for the resolution of commercial disputes, whilst the International Centre for Settlement of Investment Disputes (ICSID) is devoted to resolving investment disputes, and the Court of Arbitration for Sport (CAS) has specialized in sports-related disputes. As a very recent development, the International Centre for Energy Arbitration (ICEA) was established in 2013. In light of these specialized arbitration forums, one for the resolution of financial disputes seems logical.

This holds true all the more since the global financial crisis in 2008, when disputes arising out of financial relationships have risen dramatically. In Switzerland, the creation of a specialized arbitration court for the resolution of disputes between banks and customers has been recently discussed by parliament but finally dismissed. One argument was that financial disputes could also be resolved through the existing court system and that it was considered difficult to find experts that were both knowledgeable in banking and independent from any financial institution.

Even though the existing judicial system may be capable of settling financial disputes, expertise can produce faster and arguably fairer decisions. Certainly, a specialized tribunal would deliver a higher degree of uniform decisions and therefore provide for more legal certainty. Specialized courts may improve case management relieving the overloaded court systems experienced by many jurisdictions. They also have a more flexible system that can be adapted to the workload, either with judges who serve for limited terms or with experts that may be requested as needed.

Whether the benefits of a specialized court can balance off its drawbacks needs to be decided on a case-by-case basis. In a fast changing environment like finance, expertise providing for prompt decisions is certainly key.

2) Challenges Faced

a) Closed List of Experts

P.R.I.M.E. Finance currently provides for a list of around 80 finance and 30 dispute resolution experts from both academia and practice. Just to name two: Darrell Duffie, Finance Professor at Stanford University, and Guy Dempsey, former General Counsel at Barclay’s Capital. While the list has been expanded in March 2014, there seems to be ongoing effort to broaden or eventually open up the list.

The free choice of arbitrators ranks high amongst the top influences on the choice of an arbitration institution (38%, Graph 1) and is, therefore, an important competitive factor vis-à-vis peer arbitral institutions. The ICC Arbitration Court and the LCIA have no public list of arbitrators. This is consistent with party autonomy, a core principle in arbitration.

A system known at ICSID and the China International Economic and Trade Arbitration Commission (CIETAC) strikes a balance between the two extremes: In case the chairman of ICSID is requested to appoint arbitrators, he must choose them from the list. Similarly, the parties of a CIETAC proceeding must choose from CIETAC’s Panel of Arbitrators (around 1’000 experts), unless they agree to nominate arbitrators from outside the list (article 26).

To promote P.R.I.M.E. Finance and attract the attention from arbitrators and financial institutions alike, while guaranteeing expertise and not limiting the parties’ autonomy, such a median approach could be a sensible solution.

b) Tension between Confidentiality and Predictability

An important reason for parties to choose arbitration is confidentiality. It is common practice that arbitration proceedings are held behind closed doors. However, arbitral institutions have answered the question of confidentiality differently.

i) Publication of Awards

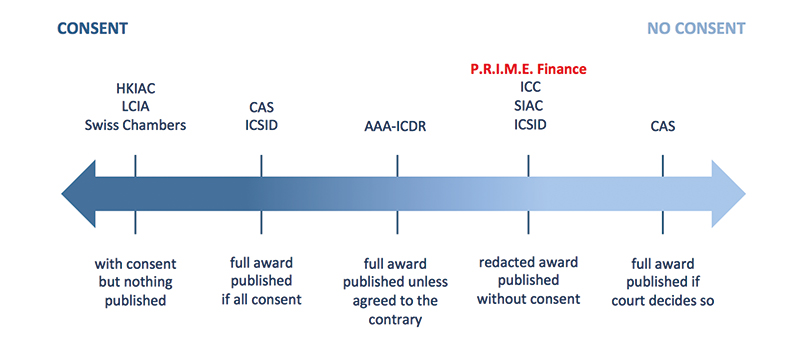

At the first glance, article 34 (5) of the P.R.I.M.E. Rules is in conformity with arbitration practice. It allows the publication of awards if all parties consent or if required by law. The latter option aims to prevent conflicts between jus cogens and the parties’ wish for confidentiality. However, what is different relates to the disclosure that is required of a party or P.R.I.M.E. Finance. Unlike other arbitration rules, the request for disclosure may also be sought from the institution itself. While the provision ultimately aims at more legal certainty, it clearly contradicts the principle of party autonomy.

But P.R.I.M.E. Finance is not the only institution that foresees the institutional publication of awards. The CAS Code, for example, states that awards shall not be made public unless all parties agree or the CAS Division President decides so (Rule 43). According to the institution, awards published on the request of the CAS Division President are very rare. In contrast to that, the ICSID Center may only publish awards with the parties’ consent (ICSID Convention article 48 (5)). In fact, most awards – which often affect entire states – are made public on its website.

The most transparent method to publish awards is in unredacted form. ICSID and CAS follow this practice. Even though it is not foreseen in the arbitration rules, the ICC regularly publishes extracts or summaries of awards in its bulletin. Recently, the Singapore International Arbitration Centre (SIAC) has commenced publicizing awards in anonymised form. To further advance a consistent body of case law but at the same time respect the parties’ wish for confidentiality, P.R.I.M.E. Finance foresees the publication of awards in redacted form.

Whether or not the parties consent is required and in which form the awards are published, can be illustrated as follows, with P.R.I.M.E. Finance being on the less consensus-oriented side:

Graph 2: Based on the respective arbitration rules

ii) Trend for Transparency

The transparency of awards could be one of P.R.I.M.E. Finance’s biggest obstacles to gain a foothold in arbitration. While the intention to enhance financial market stability is certainly valuable, financial institutions may prefer to keep their disputes secret. Since proprietary disputes between commercial parties are generally open to arbitration, their wish for confidentiality is absolutely legitimate.

Yet, transparency and cooperation requests by financial market regulators have increased since the financial crisis in 2008. Eventually, the delivery of information to the national regulator does not depend on whether the transparency of awards is explicitly enshrined in the arbitration rules or not. Arbitration confidentiality is not absolute. Even the strict confidentiality rules of the Hong Kong International Arbitration Centre (HKIAC), Swiss Chambers and ICC have to respect certain limitations imposed by law or by public policy, or limitations arising from court decisions.

Hence, the transparency rules of P.R.I.M.E. Finance are certainly ahead of the time. Whether these rules are perceived as a drawback or competitive advantage largely depends on the future developments in financial market regulation.

c) Model Arbitration Clause in the ISDA Master Agreement

In September 2013, ISDA published its first Arbitration Guide suggesting arbitration clauses of seven arbitral institutions, including P.R.I.M.E. Finance.

The hardwiring of P.R.I.M.E. Finance’s arbitration clause in the ISDA Master Agreement, a standardized contract that is used to enter into derivatives transactions on an international scale, has enormous potential. ISDA is a trade organization active in the market for over-the-counter (OTC) derivatives with more than 800 members in 67 countries. The notional amount of all outstanding OTC positions stood at USD 693 trillion in 2013, having more than tripled since 2004 (BIS Statistical Report 2013).

So far, disputes between parties of the ISDA Master Agreement have been settled before English or New York courts (article 13 (b)). The reason was the courts’ long-standing judicial experience with financial disputes. Today, many parties entering into ISDA Master Agreements are based in emerging markets and therefore the enforcement of foreign judgments may be at risk. By means of the New York Convention, allowing for a large-scale enforcement of awards, this risk can be avoided.

Confidential arbitral proceedings also prevent a precedent effect on similar market transactions. This can be of great value for large financial institutions, which can therewith avert a negative effect on similar cases. In addition, financial institutions may profit from information asymmetries, having insight into a larger number of proceedings than their private counterparties. Hence, with the publication of awards, P.R.I.M.E. Finance weakens its position considerably.

Notwithstanding the above, P.R.I.M.E. Finance is the only institution suggested in the Arbitration Guide that provides for special expertise in finance. Disputes relating to the ISDA Master Agreement can be highly complex, and, as history has shown, finance savvy courts are of high value. Considering that ISDA has published the Arbitration Guide to a large extent to guarantee the enforcement of the awards, rather than for confidentiality considerations, P.R.I.M.E. Finance’s know-how in finance is a clear advantage. The sheer market volume of OTC derivatives in combination with P.R.I.M.E. Finance’s expertise could outweigh the drawbacks.

3) What does it cost?

According to the keynote “Money makes the world go round”, arbitration costs cannot be neglected (41%, Graph 1). Arbitration costs can be divided in two categories:

1. Administrative costs (including registration fee) to manage the case, and

2. Arbitrators’ fees, which are the remuneration of the tribunal.

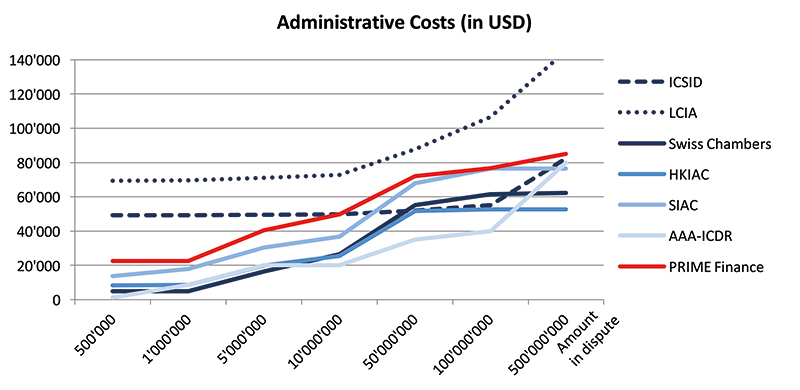

To understand P.R.I.M.E. Finance’s market position, the following graph illustrates the administrative costs in comparison to six arbitration institutions. Data of LCIA and ICSID are displayed for reference only since LCIA costs are calculated on an hourly rate (instead of an ad valorem basis), and to ISCID arbitrations different principles, such as equal treatment, apply.

Graph 3: Based on the respective cost schedules, converted into USD in May 2015

As the graph illustrates, P.R.I.M.E. Finance is priced slightly higher than the other arbitral institutions. This may be explained by the absence of economies of scale. While high administrative costs can deter parties, high costs may also be seen as a seal of quality and therewith attract complex cases.

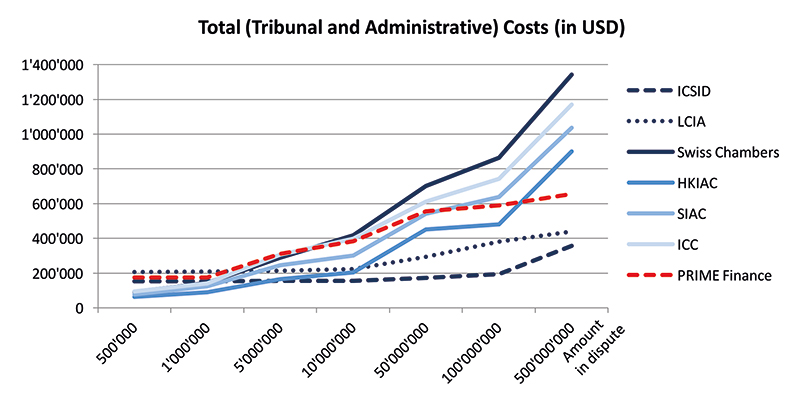

The determination of arbitrators’ fees leaves P.R.I.M.E. Finance to the discretion of the tribunal. In relation to the total costs of six other arbitral institutions and based on P.R.I.M.E. Finance’s administrative costs, the following graph shows a prospective trend line of P.R.I.M.E. Finance’s total costs.

Graph 4: Based on the Global Arbitration Review 2013 and the respective arbitration rules

As illustrated above, the Swiss Chambers have the highest total costs, followed by the ICC and SIAC. In relation to their competitors, the total costs for P.R.I.M.E. Finance are estimated to be higher in lower, and clearly lower in ascending amounts in dispute. The estimated trend for P.R.I.M.E. Finance’s total costs may be explained by the assumption that the complexity of disputes does not depend on the amount in dispute, resulting in relatively consistent arbitrators’ fees.

Relative to its competitors, the estimated total costs make P.R.I.M.E. Finance an attractive choice when medium to high amounts are in dispute. Nevertheless, this trend line is only an estimate, leaving the parties with certain insecurity when it comes to the arbitrators’ fees.

4) Conclusion

Even though exposed to certain criticism, P.R.I.M.E. Finance has potential in the settlement of financial disputes. To further increase its attractiveness, P.R.I.M.E. Finance may open up its closed list of experts. With the advantage to enforce arbitral awards internationally, together with its expertise in finance, P.R.I.M.E. Finance is poised to take a strong position among the international arbitration regimes. The greatest challenge relates to the transparency of awards and that market participants gain confidence in P.R.I.M.E. Finance. If cooperation efforts by public authorities in financial markets rise, and P.R.I.M.E. Finance successfully hardwires its arbitration clause into financial contracts on a larger scale, it may expect a busy future.

Désirée Klingler (desiree.klingler@bluewin.ch)