Withholding Tax on Interest to be Replaced by Paying Agent Tax System

The Swiss Federal Council issued a proposal on 17 December 2014 to replace the current withholding tax on interest payments by a new paying agent tax system. The new system would be applicable to both domestic and foreign issued bonds and debentures. A Swiss paying agent would have to withhold the Swiss withholding tax, if the payment would be made to a domestic individual. Payments to domestic entities as well as payments to foreign persons would be out of scope of the Swiss withholding tax system.

By Stefan Oesterhelt (Reference: CapLaw-2015-5)

1) Current law

Under the current law interest paid by a Swiss resident borrower is not in principle subject to Swiss withholding tax (Verrechnungssteuer) of 35%, unless the instrument under which interest is paid is classified as a “bond” (Anleihensobligation), a “debenture” (Kassenobligation) or a “deposit” (Kundenguthaben) for Swiss withholding tax purposes.

The Swiss withholding tax has to be paid by the issuer of such bond, debenture or deposit to the Swiss Federal Tax Administration. The bondholder or creditor has the possibility to reclaim the Swiss withholding tax based on internal law (if it is a Swiss resident person) or based on a double taxation treaty.

The interest component of structured products issued by a domestic entity as well as retained profits and distributions of domestic mutual funds (unless they derive from capital gains) are also subject to 35% Swiss withholding tax.

2) The Proposal of 17 December 2014

The new withholding tax law proposed by the Swiss federal council on 17 December 2014 will replace the current withholding obligation of the issuer (or the Swiss guarantor, as the case may be) for a withholding obligation of Swiss paying agents. Swiss paying agents will have to remit 35% withholding tax to the Swiss federal tax administration if the interest is paid to a Swiss resident individual in the following cases:

-

Bonds and debentures issued by a Swiss or foreign resident entity (irrespective whether the proceeds of a foreign issued bond will be used in Switzerland or not);

-

Interest component of structured products issued by Swiss or foreign resident entity;

-

Interest component of distributions and retained profits by Swiss and foreign mutual funds;

-

Interest payments on bank deposits.

The new paying agent tax will also apply to bonds which are currently exempt from Swiss withholding tax such as CoCo-Bonds and Write-Down-Bonds.

No distinction will be made between Swiss and foreign issued bonds, debentures, structured products and mutual funds.

3) Function of Swiss Paying Agent

The paying agent, i.e., any person who within the conduct of its business regularly or occasionally remits, transfers or credits interest in connection with bonds and debentures (as defined), or collects such interest for third parties, will be responsible for determination whether a payment constitutes a taxable interest payment and be liable for the tax to be deducted, in the worst case for the grossed-up tax amount. In addition, the paying agent will have to deduct withholding tax on the accrued interest also in the case of a sale of such bond. This is fundamentally new, as accrued interest components are currently generally not subject to the withholding tax.

The paying agent will also be responsible for determining whether the exemption for foreign investors applies, i.e., whether the beneficial owner is resident outside Switzerland. If the paying agent has any doubt about the identity of the beneficial owner he will be required to withhold.

Accordingly, the tasks of Swiss paying agents are sensible and demanding. If the Swiss federal tax administration in an audit concludes that the Swiss paying agent did not withhold tax as required, the paying agent will be liable for tax not withheld, as mentioned earlier, in the worst case on the grossed-up amount.

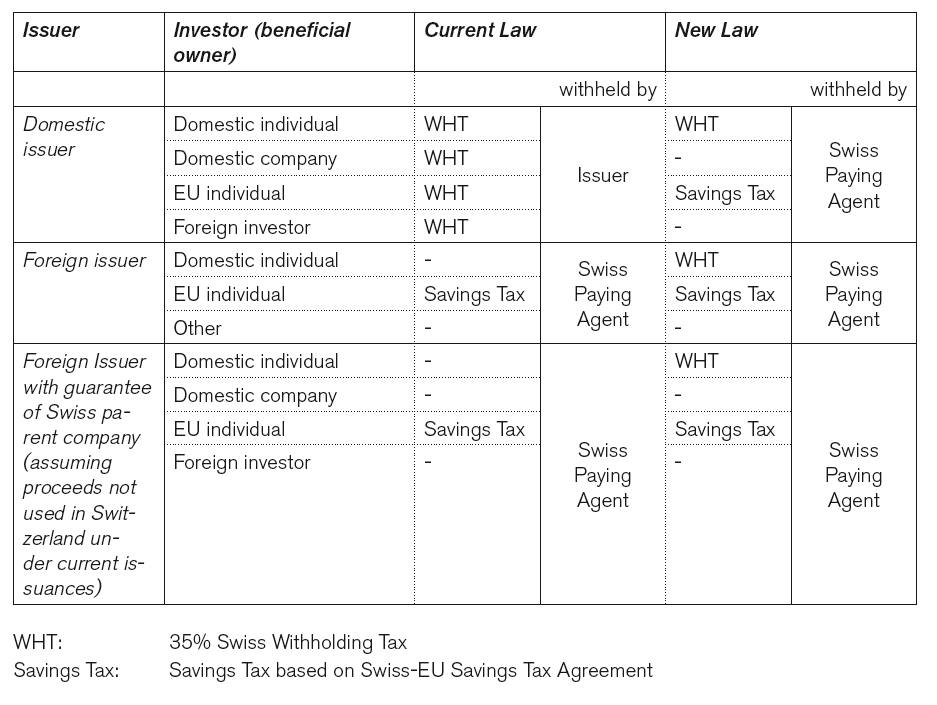

4) Comparison of Current Law and Proposed New Law

The diagram below compares the basic Swiss withholding tax situation under the current and the new law and includes the EU Savings Tax:

Stefan Oesterhelt (stefan.oesterhelt@homburger.ch)