FinTech Regulation (2.0): An Overview on the Proposed Three Element Solution

More regulation and digitization are two important trends that are currently reshaping the financial industry in Switzerland. In this context, the Swiss Federal Council has proposed the creation of a specific new FinTech regulation that shall be particularly relevant for business models in the overlapping areas of these two topics and has mandated the Federal Department of Finance (FDF) to develop a consultation draft that further specifies the “Three Element Approach” of the Swiss Federal Council. On 1 February 2017, the FDF published its related Explanatory Report on the Amendment of the BA and BO (FinTech). This article contains a short overview of the key parameters of the proposed new Swiss FinTech regulation and a first view on the Explanatory Report.

By Luca Bianchi (Reference: CapLaw-2017-02)

1) Introduction

Currently, there are two major action points of strategic importance on the agenda of every financial services or products provider in Switzerland: regulation and digitization. The topic FinTech lies at the very essence of these two trends. While regulation tends to be backwards looking, digitization represents a view in the future. The problem is that these two major trends may, sometimes, be incompatible with each other. In the past year, developments regarding FinTech regulation have happened very fast (see CapLaw-2016-31, 3). However, the most important milestones in terms of Swiss FinTech regulation are yet to come.

In particular, the next major step will, presumably, be the implementation of a proposed new and specific FinTech (de)regulation. The Federal Department of Finance (FDF) published its Explanatory Report on the Amendment of the BA and BO (FinTech) on the proposed new FinTech regulation on 1 February 2017. After completion of the consultation proceeding, there will likely be certain differences between the content of this article when compared with the result of the consultation (once available).

In the meantime, this article provides a brief overview on the ongoing structural regulatory changes as well as a summary of the expected FinTech specific regulatory developments.

2) Structural Regulatory Changes aim for FinTech Unicorns

a) The Old World: Financial Market Regulation vs. Tech Craze

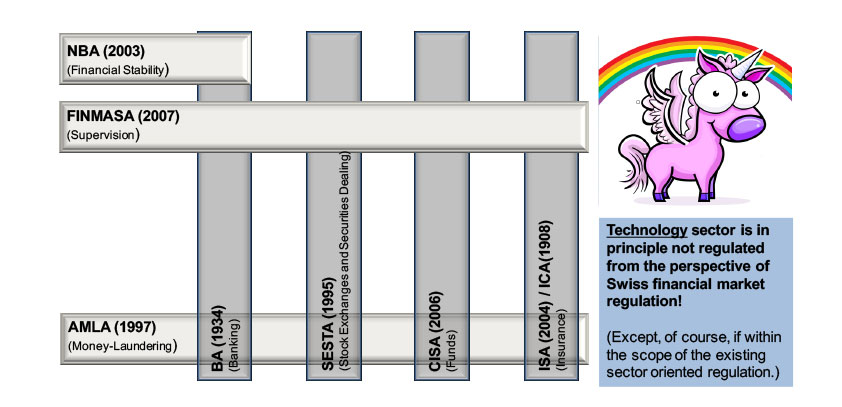

i. Overview of the Regulatory Framework (1.0)

The following graph describes the “old” sector oriented Swiss financial market architecture and its relationship to technology companies.

(Source: Sandro Abegglen / François M. Bianchi / Luca Bianchi et al., Switzerland’s New Financial Market Architecture, 2nd edition, Zurich 2016, p. 19, modified version)

ii) Explanation of Selected Aspects

In the “old world”, financial services and technology companies where mostly allocated to separate industry sectors. During and after the tech bubble of the nineties (and the rise of the internet), new global technology companies such as Facebook, Uber, Airbnb or Apple, which were subject to a very strong growth, were founded or further developed.

From a Swiss financial market regulatory perspective, typical technology companies were generally not subject to financial market regulation unless they intended to operate within the scope of the traditional sector-oriented regulation, which was rarely the case.

By creating and exploring new markets free from or with less rigid jurisdiction specific regulations and restrictions, many tech companies were able to experience exponential growth and to establish a global presence. Such prosperous tech startup companies are frequently called “unicorns” and are shining examples of success stories in entrepreneurial circles.

In contrast thereto, financial services and products providers were traditionally subject to very rigid and fragmented local regulations, in particular, in Switzerland and in Europe (but also in many other countries).

The “lean” startup approach suggests that overplanning, the generation of large expenses, or long product development periods are avoided for early stage digital products or startups. Thus, a typical tech startup frequently tries to enter the specific online target market very quickly with an already functioning but not completely “finished” Minimum Viable Product (MVP).

As of today, from a regulatory perspective it is not permitted to enter the FinTech market without fulfilling all the applicable regulatory requirements (if any) from the very beginning. In a worst case scenario, the going live of an MVP may not be in line with Swiss financial market regulation and can, potentially, be subject to regulatory or penal sanctions. Therefore, it is recommended to make an appropriate effort to evaluate each FinTech business model from a regulatory perspective before the launch of the MVP.

b) The New World or Unicorns in the Labyrinth

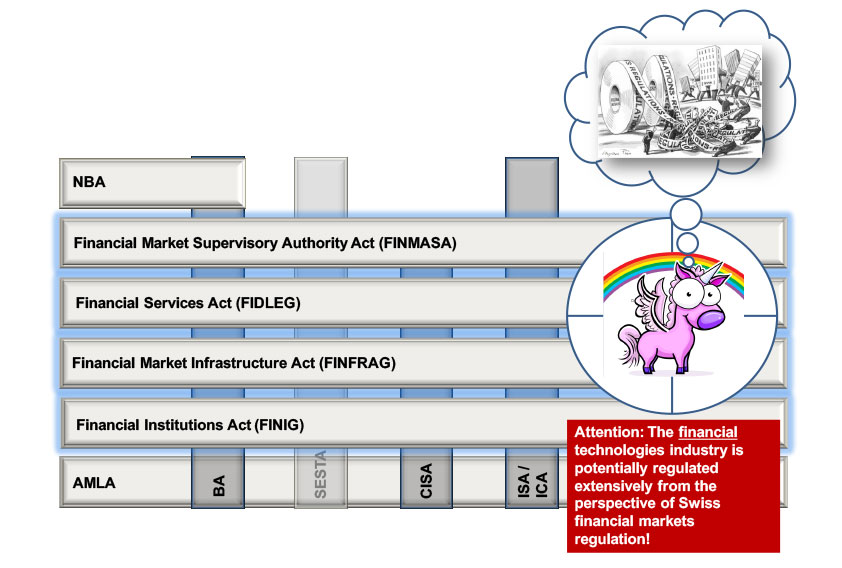

i. Overview of the Regulatory Framework (2.0)

The “new” topic oriented cross-sector Swiss financial market architecture that is in the process of being implemented in Switzerland has the (unintended) side effect of hindering innovative FinTech startups even more extensively as set out in below graph.

(Source: Abegglen / Bianchi / Bianchi, loc. cit., p. 22, modified version)

ii. Explanation of Selected Aspects

Unlike typical tech startups, a FinTech startup may be subject to the traditional financial market regulation that has historically been created for banks, stock exchanges, securities dealers or collective investment schemes, for the respective mature industries and based on experiences in the past (e.g., cases of damages, losses, defaults, or fraud).

In particular, licensing requirements, minimum capital requirements, accounting requirements, substance requirements, KYC-duties or other regulatory requirements for traditional financial services providers can, potentially, put an end, slow down or significantly complicate the development, testing, launching and scaling of an MVP in the FinTech market.

Against this background, FinTech startups seem to be caught and hindered by a labyrinth of existing and proposed new regulations that are frequently very hard to understand or even entirely incomprehensible for FinTech entrepreneurs.

Thus, financial market regulation can be a significant market entrance barrier for new market participants in the FinTech industry.

3) The Proposed Swiss FinTech Regulation (2.0)

a) A Three Element Solution

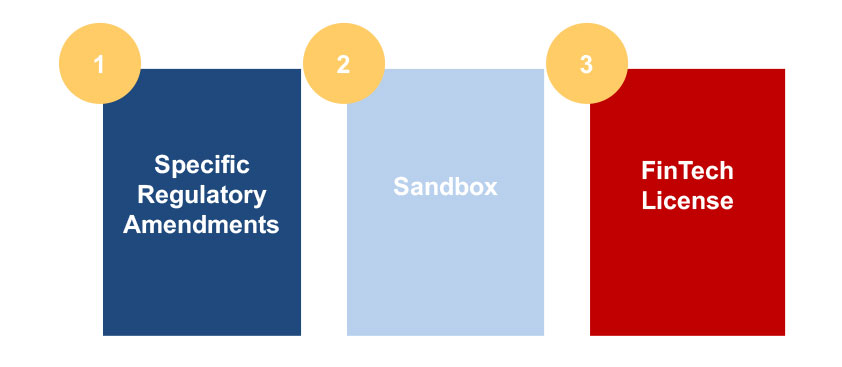

The Swiss Federal Council alongside the FDF is in the process of developing a model for a proposed FinTech (de)regulation that will, presumably, be based on its current “Three Element Approach” as described in the following graph.

(Source: FDF, Background documentation on the reduction of barriers to market entry for FinTech firms, 2 November 2016, free translation, available under https://www.admin.ch/gov/en/start/documentation/media-releases.msg-id-64356.html (last visited on 16 January 2017), p. 2)

The existing regulatory framework does frequently not “fit” or is not “adequate” for FinTech business models and the needs and expectations of new market participants in the FinTech space (i.e., there exists a regulatory mismatch). In addition, the question of regulation or deregulation of FinTech represents a true regulator’s dilemma.

The new Swiss Three Element Approach is a possible solution for such a regulator’s dilemma. The three elements of this approach are described in further detail in the next paragraph.

b) The Three Elements

i. Specific Regulatory Amendments (Element 1)

With respect to specific regulatory amendments, a special focus lies on the extension of the timeframe for settlement accounts. Currently, credit balances on certain client settlement accounts (e.g., with securities dealers, precious metal traders, asset managers or any similar firms) are not considered to be deposits (article 5 para. 3 lit. c of the Banking Ordinance (BO)).

These types of settlement accounts set forth that the accounts exclusive purpose is to serve the settlement of client transactions and that no interest is paid on the deposits. This exception shall also be applicable for accounts of FinTech companies. However, in this context, the requirement that a settlement account exist for a maximum period of seven days poses a problem. Fundraising for crowdfunding projects typically takes longer than that. Thus, a timeframe of 60 days shall newly be implemented for settlement accounts in the BO.

In addition, the Swiss Federal Council of States has attempted to make another specific regulatory amendment concerning the support of innovation in the proposed new Art. 1abis of the Banking Act (BA) in the process of dealing with the draft Financial Services Act (FIDLEG) and Financial Institutions Act (FINIG). However, the proposed wording seems to have been integrated in the Explanatory Report on the Amendment of the BA and BO (FinTech) of 1 February 2017 and the respective draft provisions (see Point 4 below). Thus, consistency between the legislative process concerning the FIDLEG and FINIG and the new FinTech regulation should be ensured.

In conclusion, particularly crowdfunding platforms could benefit from the proposed specific regulatory amendments. As long as crowdfunding platforms will accept client money only within the extended timeframe set out above, they should, presumably (and under the reservation of other potentially applicable regulatory restrictions), not be subject to the banking license requirement or the anticipated new FinTech license requirement.

ii. Regulatory “Sandbox” (Element 2)

The regulatory “sandbox” is essentially an expansion of activities that are exempt from a licensing requirement. At the moment, client deposits can be accepted from a maximum of 20 people without triggering regulatory licensing requirements.

Many FinTech business models aim to address the general public or at least more than 20 people. The element of a sandbox will enable a provider without a banking license to accept public funds within the quantitative threshold of a total amount of up to CHF 1 million, but without the application of a threshold that relates to the number of depositors.

The acceptance of public funds above this threshold would be subject to a separate approval by FINMA; either by granting a full-fledged banking license or, more likely, the new FinTech license (see below).

Thus, the sandbox has the purpose to permit the limited market testing of MVPs without the market entry barrier of a banking license (or even a FinTech license) to the extent that a FinTech provider operates within the defined limitations of this innovation space.

However, FinTech providers that are operating within the scope of the sandbox will have to inform clients that the company is not supervised by FINMA for transparency purposes. In addition, they must still comply with the potentially applicable anti-money laundering regulation.

iii. FinTech License (Element 3)

The actual breakthrough is certainly the proposed FinTech license that represents a new category of a regulatory status for FinTech providers that do not provide typical banking activities, but whose business includes only certain elements of banking (and, therefore, has a lower risk profile).

FinTech institutions that aim to perform a deposit-taking business and do not execute a credit business with maturity transformation may be subject to this new licensing requirement. Under the FinTech license, public deposits may not exceed the total amount of CHF 100 million. If client protection is ensured, FINMA may authorize a higher threshold.

The deposits must be held on one or more accounts and in the name of the license holder. No interest may be paid on such deposits. The minimum capital requirement for such regulated FinTech institutions shall be 5% of the accepted deposits and at least CHF 300,000.

Consequently, the proposed new FinTech license will, presumably, reduce regulatory (market entry) barriers for many FinTech providers, in particular, in the area of crowdfunding, blockchain, and digital payments.

4) A First View on the Explanatory Report on the Amendment of the BA and BO (FinTech) of 1 February 2017

a) Preliminary Remark

The FDF published its Explanatory Report on the Amendment of the BA and BO (FinTech) on 1 February 2017. It can be downloaded on https://www.admin.ch/gov/ en/start/documentation/media-releases.msg-id-65476.html (last visited on 1 February 2017).

The following section of the text represents a brief summary of a first review of the Explanatory Report.

Firstly, the Explanatory Report contains a general overview on the FinTech industry and explanations concerning the most important FinTech business models such as crowdfunding, digital payment systems, blockchain applications, robo advisers, and digital asset management.

Secondly, the Explanatory Report describes the currently applicable financial market regulation and the general need to adapt it to the digital age.

Thirdly, specific amendments to the BA as well as to the BO are suggested in line with the proposed Three Element Solution and as further described below.

b) Key Points

i. Proposed Amendments to the BA

A proposed new article 1a BA aims to introduce an amended definition of the term “banks”. In addition, the proposed new article 1b para. 1 BA provides for a general application by analogy of the BA (which shall be subject to certain exceptions as described below) on financial services providers (FinTech license) that:

- accept deposits of up to CHF 100 million from the public or solicit such deposits publicly; and

- neither invest such public deposits nor pay interest on them.

In addition, the Swiss Federal Council may reduce this threshold based on certain considerations, including the competitiveness and innovative capacity of the Swiss financial center.

However, the following special provisions and exceptions to the general rule set out above shall apply:

- Reduction of accounting obligations: Instead of the stricter accounting rules for banks, the general accounting rules of the Code of Obligations (CO) shall be applicable to FinTech providers that are in the scope of article 1b para. 1 and 3 BA.

- Reduction of audit requirements: Rather than the stricter audit requirements for banks, the audit rules of the CO shall be applicable for FinTech providers that are subject to these rules.

- Examinations by licensed audit companies: With respect to an examination under article 24 Financial Market Supervisory Authority Act (FINMASA), FinTech providers must mandate a licensed audit company.

- Reduction of rules for bank deposits: With respect to explicitly permitted types of deposits with FinTech providers, the provisions regarding privileged deposits and immediate outpayments for banks shall not be applicable.

In special cases, FINMA may decide that the above provisions also apply for FinTech providers that: (i) exceed the threshold of CHF 100 million or solicit deposits publicly or (ii) do not accept deposits from the public and apply for a license.

Furthermore, the proposed new article 47 para. 1 lit. a BA introduces a professional secrecy for FinTech providers which is similar to the existing banking secrecy. Intentional or negligent breaches of the professional secrecy for FinTech providers can, presumably, be punished with imprisonment of up to three years or a financial penalty.

ii. Proposed Amendments to the BO

The proposed amendments to the BO comprise the following two carve outs:

- Carve out from the existing legal term “deposits”: Credit balances on settlement accounts of clients with securities dealers, commodity traders, asset managers or similar companies (i.e., FinTech providers) shall explicitly not qualify as deposits if no interest is paid thereon and the settlement is made within 60 days (specific regulatory amendment).

- Carve out from the term “commercial nature”: Whoever is mainly active in the financial industry and accepts or publicly solicits deposits does not act with a commercial nature, if he accepts such public deposits within a maximum threshold of CHF 1 million and does not pay interest thereon (sandbox).

In addition, clients must be informed if the FinTech provider is not supervised by FINMA and the deposit is not subject to the legal deposit guarantee.

c) Initial Findings

In a nutshell, the Explanatory Report contains a specified proposal on how to implement the new FinTech regulation (Three Element Solution) described above in the existing Swiss banking regulation. It seems to overtake certain amendments that have already been suggested to the BA and BO during the legislative process regarding the FIDLEG and FINIG. Furthermore, it combines these elements with more detailed aspects of the proposed new FinTech regulation.

It is somehow surprising that the new FinTech regulation shall not be inserted into the FIDLEG and FINIG (including a general non-application of the BA and BO instead of an introduction of a number of exceptions thereof). This would seem to be a more liberal and, thus, better solution to introduce general rules on the regulation and supervision of FinTech providers.

Nevertheless, it cannot be excluded, that the reason for the selected approach may have been a question of timing and the decision was made under consideration of the earliest possible date of entering into force of the new FinTech regulation (which could, potentially, be subject to a delay if the new rules would be integrated in the FIDLEG and FINIG).

Against this background, the selected approach may be considered to be pragmatic and a very smart move by the legislator. However, it could certainly make sense to establish a more sophisticated Swiss FinTech regulation in the FIDLEG and FINIG (as well as in the Financial Market Infrastructure Act (FINFRAG)) at some point in the future.

5) Conclusion and Outlook

In a strictly regulated industry such as the financial industry the way out of the regulatory mismatch and the regulator’s dilemma seems to be a punctual deregulation of financial services and products in the FinTech space. In particular, such liberalization should have the purpose to create adequate rules that are suitable for new business models, to ensure minimal professional standards, and to clarify the regulatory status as well as regulatory requirements and duties for market participants in the FinTech space. The current Three Element Approach represents a remarkable step in the right direction.

The consultation process with respect to the proposed FinTech regulation will last until 8 May 2017. The exact timeline with respect to the further implementation of the proposed new FinTech regulation is not clear at this point in time. Nevertheless, it is essential to implement the new rules as soon as possible in order to compete successfully with other leading FinTech locations that aim for a liberalization of the FinTech industry in their countries in the near future as well.

Luca Bianchi (luca.bianchi@nkf.ch)