New Swiss financial market regulation: Consequences on pension funds, investment foundations, their asset managers and advisors

The new Swiss financial market regulation will take effect in the second half of 2019 or in 2020. The new acts, namely the Financial Services Act and the Financial Institutions Act are particularly relevant to external asset managers of pension funds and investment foundations. The pension funds and investment foundations themselves will not be directly impacted, but will indirectly benefit from increased conduct and transparency rules and the fact that their external asset managers henceforth will be subject to supervision by FINMA or a FINMA-authorized supervisory organization.

By Sandro Abegglen / Evelyn Schilter (Reference: CapLaw-2018-04)

Since 1 January 2014, external persons and institutions may only be entrusted with the asset management of pension funds if they are subject to supervision by a financial market authority or have been granted a permit by the Federal Supervisory Commission Occupational Pension Benefits (Oberaufsichtskommission Berufliche Vorsorge OAK BV). In essence the permit by the OAK BV consists of a one-time review of the fit and proper status (Gewährsprüfung) on the occasion of granting the permit (which is limited to three years and can be renewed) as opposed to a continuous supervision as carried out by FINMA, for example. An asset manager qualifies as someone who holds a power of attorney for the independent, discretionary investment of pension assets, or the purchase or sale of real estate, but not an advisor, real estate manager, or real estate agent. An asset manager must, in particular, have a good reputation, guarantee proper business conduct, and be free of conflicts of interest (see article 51b of the Occupational Pension, Survivors’ and Disability Benefits Act (OPA)). The legislator thereby wanted to ensure competent and professional asset management in the field of occupational pension benefits, where large sums are held in trust.

Within the new Swiss financial market regulation, external asset managers previously subject to the authorization by the OAK BV shall now also become subject to continuous financial market regulation supervision by FINMA or a FINMA-authorized supervisory organization and shall be required to satisfy certain requirements, particularly regarding rules of conduct and organization. This new regime is expected to come into effect in the second half of 2019 or in 2020. As such, this article is based on the drafts of the Financial Services Act (FinSA) and the Financial Institutions Act (FinIA) pursuant to the dispatch of the Federal Council dated 4 November 2015, as modified by the Council of States on 14 December 2016 and by the National Council on 13 September 2017.

1) FinSA and FinIA as part of the new Swiss financial market infrastructure

The FinSA and FinIA are part of the new Swiss financial market infrastructure, which consists of the following areas (i) supervision (Federal Act on the Swiss Financial Market Supervisory Authority (FINMASA) dated 22 June 2007 and already in effect), (ii) infrastructure (Financial Markets Infrastructure Act (FMIA) dated 19 June 2015 and already in effect), (iii) services (FinSA), and (iv) controlled institutions (FinIA). The FinSA contains rules about the offering of financial services and the marketing of financial instruments across sectors. These rules follow largely the EU regulations (MiFID II, Prospectus Directive, project PRIIP). The goal is to establish an equivalent regulation, but also one that takes the Swiss circumstances into consideration. Requirements for the loyal, diligent, and transparent delivery of financial services are outlined in the rules. Specifically, financial service providers will have to abide by supervisory rules of conduct, particularly with regard to duties of information and of appropriateness and suitability, which will be tiered by client segments. The FinSA distinguishes between private clients, professional clients and institutional clients.

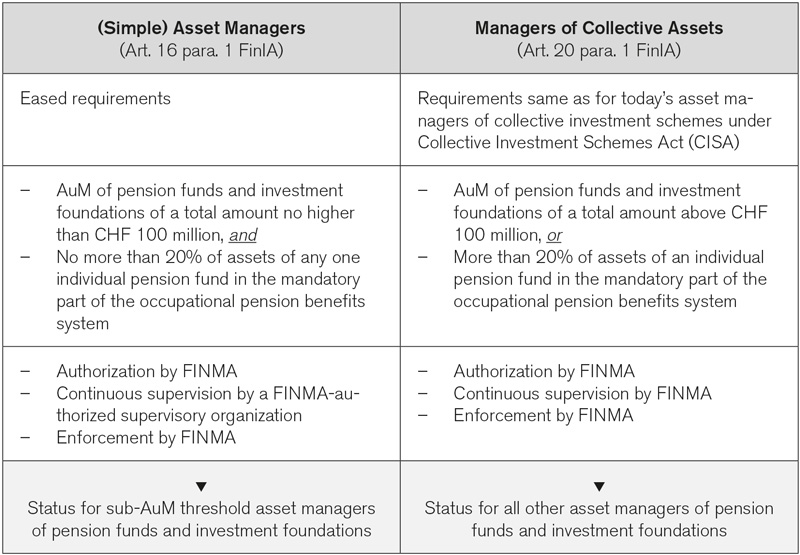

The FinIA will regulate the institution-related requirements of all financial service providers (except banks and insurers, which remain regulated by their existing regimes, i.e., the Banking Act, Insurance Supervision Act, but will also be subject to FinSA). All financial service providers will be subject to licensing by FINMA, specific authorization requirements and ongoing supervision by FINMA, directly or by a FINMA-authorized supervisory organization. With regards to the organizational and financial requirements for a license, distinctions are made between simple asset managers, managers of collective assets, fund management companies and investment firms.

Both laws aim to create consistent competitive conditions, improve customer protection, promote the international competitiveness of Switzerland as a financial center, and stipulate certain penal sanctions in case of infringements.

The Federal Council adopted the dispatch on the FinSA and the FinIA on 4 November 2015. The bill is currently under consideration in parliament, with deliberations concluded both in the Council of States and the National Council. Currently, the procedure for reconciling the positions of the Council of States and the National Council is ongoing. It is planned that the bill will be further deliberated by the Council of States and that remaining differences will be reconciled thereafter. Accordingly, certain changes to the version as resolved by the National Council on 13 September 2017 will take effect and it is to be expected that both laws will not go into effect before the second half of 2019 and that the accompanying implementing ordinances will only be available towards the end of 2018 or early 2019.

2) What is new for asset managers?

External managers of assets of pension funds and investment foundations pursuant to article 53g OPA will become subject to FINMA licensing and financial market regulations, as is the case for asset managers of investment funds or simple asset managers – i.e. their special regime as described above with OAK BV registration will be abandoned. In principle, they will qualify as more strictly regulated managers of collective assets subject to FINMA supervision. The less regulated status of the (simple) asset managers on the other hand is legally designed as an exception for “small” asset managers.

Aside from the institution-related permit requirements, the adherence to which will now continuously be supervised, both types of asset managers will need to abide by the FinSA’s rules of conduct in the future (see below); infringements will result in regulatory and partly criminal sanctions.

The most important rules of conduct for external asset managers under the FinSA are duties of information, the obligation to conduct an appropriateness and suitability test, duties of documentation and accountability and the duty to avoid conflicts of interest. The latter includes the duty to fully pass on any third party compensation (retrocessions, etc.) to the client, unless the client has previously been explicitly informed about and has waived such third party compensation.

It is to be expected that the heightened requirements on external managers of pension funds and investment foundations will result in a certain consolidation amongst external asset managers. At the same time, they will also gain improved opportunities of access to the European market.

It should be noted that the new regime will only apply to external asset managers of pension funds and investment foundations. For the supervision of pension funds, investment foundations, and their adherence to investment management requirements under pension and investment foundation laws, the cantonal supervisory authorities or the OAK BV, respectively, will remain the competent authorities. This results in a certain parallelism of the various supervisory activities by different authorities. These overlapping supervisory activities will likely result in certain delimitation issues.

3) Consequences for pension funds and investment foundations

Under the FinSA, pension funds and investment foundations are not considered institutional clients. Rather, they are considered professional clients if they have a professional treasury, or private clients otherwise (see article 4 FinSA). According to the dispatch of the Federal Council on FinSA and FinIA dated 4 November 2015 (p. 8949), a professional treasury exists if the pension fund or investment foundation entrusts at least one experienced financial expert with consistently managing its financial resources. Thus, pension funds whose assets are managed exclusively externally are considered private clients, and they therefore benefit from the highest possible customer protection under the FinSA. It remains to be seen whether banks and brokers may also qualify a pension fund or investment foundation with an external asset manager as professional client.

Opting out of the private client segment into the segment of professional clients will be possible under certain circumstances. If pension funds are considered professional clients, they can also declare that they want to be considered institutional clients. Opting into the private client segment and therefore a higher level of protection will always be possible for professional clients.

Disputes regarding legal claims between a pension fund or investment foundation and an external asset manager can be brought before an ombudsman’s office and will be dealt with in a proceeding that is non-bureaucratic, fair, quick and cost effective for the pension fund or investment foundation. Recourse to the courts is thereby not excluded. Thus, as a result of the new rules the legal protection for the pension funds and investment foundations will likely be improved.

As mentioned, the pension funds themselves, as opposed to their external asset managers, will not be subject to the FinIA and will thus not be considered financial institutions pursuant to the FinIA, therefore not needing a respective FINMA license. The same is true for investment foundations. However, pension funds and investment foundations will henceforth need to verify that their external asset managers are in possession of the necessary FINMA authorizations.

Asset managers and portfolio managers who are employed by a pension fund or investment foundation will not be subject to authorization requirements according to the FinIA, nor will they be subject to the rules of the FinSA. However, it may not be excluded that the heightened requirements on external asset managers will indirectly raise the requirements on internal asset managers as well. The foundation board and management of a pension fund will need to take this development into account within the scope of their legal duties in connection with the management of pension fund assets under the occupational pension benefits law.

4) Note on (investment) advisors

Advisors who provide advisory services that qualify as financial services as defined by the FinSA (typically investment advisory services) without being regulated themselves as (simple) asset managers or higher, will not be subject to supervision, but they will have to be registered in an advisors’ register. In addition they will have to abide by the FinSA’s rules of conduct, the breach of which will be punishable.

This regime will result in issues of delimitation toward the “top”, i.e. toward regulated asset managers (be it simple ones or managers of collective assets), but also toward the “bottom”, i.e. toward such advisors of pension funds or investment foundations who do not provide financial services according to the FinSA.

5) Need for action

Pension funds and investment foundations can and must make use of the upcoming changes and take the opportunity to examine the pros and cons of internal and external asset management and to adapt existing solutions if necessary and/or to review their external asset management mandates and modify them if need be.

Smaller external asset managers should determine under which asset manager status they will want or have to provide their services in the future and make the appropriate adjustments to their business model.

Bigger asset managers who will be considered managers of collective assets should check to what extent the new regulations contain additional requirements and plan for the necessary adjustments.

Advisors should first assess whether they provide financial services according to the FinSA, particularly investment advice, in order to gain clarity about their future status. Secondly, they should evaluate whether they do, de facto, provide asset management services, in which case the two preceding paragraphs are relevant.

Sandro Abegglen (sandro.abegglen@nkf.ch)

Evelyn Schilter (evelyn.schilter@nkf.ch)

This is an updated and modified version of an article by the authors on the subject matter published in Schweizer Personalvorsorge, 09/17, p. 97 et seq