New Limited Qualified Investor Fund (L-QIF) – Innovation and Deregulation as Growth Catalyst for the Fund and Asset Management Industry in Switzerland

The Federal Council aims to boost the attractiveness of Switzerland as a domicile for fund production with the proposed introduction of the Limited Qualified Investor Fund (L-QIF). The ongoing consultation period for the L-QIF was initiated on 26 June 2019 and will end on 17 October 2019. The L-QIF is an innovative financial product that may invest in all thinkable investments and will benefit from very flexible investment restrictions. To speed up time-to-market and reduce costs, the L-QIF will neither require a regulatory authorization or product approval nor will it be subject to ongoing supervision by the Swiss Financial Market Supervisory Authority FINMA.

By Sandro Abegglen / Luca Bianchi (Reference: CapLaw-2019-41)

1) Introduction

Good news for the Swiss funds and asset management industry: the Federal Council intends to increase the attractiveness of Switzerland as a fund production location by introducing the new Limited Qualified Investor Fund (L-QIF) in the Collective Investment Schemes Act (CISA). The L-QIF is a collective investment scheme which is accessible exclusively for qualified investors. It must be administrated in accordance with the requirements of the CISA. However, the L-QIF shall – most importantly – not require an authorization or an approval by the Swiss Financial Market Supervisory Authority FINMA.

The development of the L-QIF has been shaped and pushed forward by the Swiss Funds & Asset Management Association SFAMA as well as the Federal Council, respectively, the Federal Department of Finance (FDF). As a result, the FDF has published a Preliminary Draft of the new CISA-provisions regarding the L-QIF (the Preliminary Draft or PD) as well as an Explanatory Report to the Preliminary Draft concerning Amendments to the Collective Investment Schemes Act (the Explanatory Report) on 26 June 2019. The consultation period will end on 17 October 2019.

2) Overview

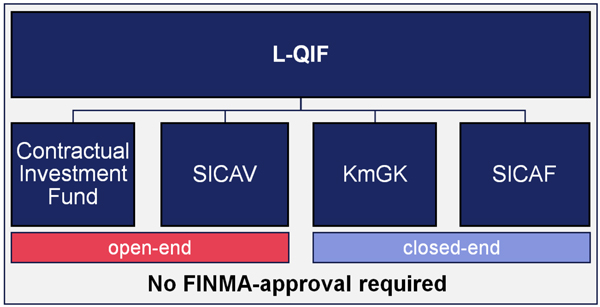

The following chart shows the structuring options for an L-QIF:

The above graph indicates that the L-QIF can be set-up in the form of open-end structures such as the contractual Investment Fund or the Investment Company with Variable Capital (SICAV) or closed-end structures such as the Limited Partnership for Collective Investment (LP, respectively, KmGK), or the Investment Company with Fixed Capital (SICAF). Thus, it must be launched in one of the existing legal forms of the CISA (but does not require a FINMA-approval).

3) Key Points

The L-QIF features the following key points:

– Only for qualified investors: The L-QIF will be accessible exclusively for qualified investors (article 118a(1) lit. a PD-CISA in connection with article 10(3) CISA and article 4(3-5) FinSA) such as:

– Financial intermediaries as defined in the BA, the FinIA and the CISA;

– insurance companies;

– foreign clients subject to prudential supervision (like the Swiss financial intermediaries listed above);

– central banks;

– public entities with professional treasury operations;

– occupational pension schemes and entities which serve the aim of occupational pension schemes with professional treasury operations;

– companies with professional treasury operations;

– large companies (i.e., companies that exceed two of the following thresholds: (i) balance sheet total of CHF 20 million, (ii) sales revenue of CHF 40 million, or (iii) equity of CHF 2 million); and

– investment structures with professional treasury established for high-net-worth (HNWI) private clients.

Furthermore, HNWI (and private investment structures without professional treasury established for them) which declare that they wish to be treated as professional clients (opting-out) according to article 5(1) FinSA are deemed to be qualified investors (article 10(3) CISA). In addition, investors with a permanent written asset management or investment advisory agreement which are considered qualified investors in terms of the CISA are admitted to invest in an L-QIF, unless they declared in writing that they want to be treated as retail clients (article 10(3) CISA). Non-qualified investors are not allowed to invest in an L-QIF.

Attractively, as any other Swiss fund, an L-QIF can be set-up as a single investor fund for insurance companies, public entities with professional treasury operations, occupational pension schemes, or entities which serve the aim of occupational pension schemes with professional treasury operations (article 7(3) CISA; article 5(4) D-CISO; Explanatory Report, p. 33).

– Investment restrictions: Special and very liberal investment restrictions apply for the L-QIF (article 118n et seq. PD-CISA). The investment restrictions of the supervised fund structures listed in the overview in section 2 are, in principle, not applicable for the L-QIF (Explanatory Report, p. 16). Generally speaking, all thinkable investments are permitted for an L-QIF (within the legal system) (Explanatory Report, p. 27). In particular, the Explanatory Report expressly mentions securities (Effekten), units of collective investment schemes, money market instruments, real estate, derivatives, structured products, commodities, infrastructure projects, crypto currencies, wine, art, or old-timers as examples of feasible investments of an L-QIF. Furthermore, the PD-CISA does not contain regulatory diversification requirements (article 118o PD-CISA; Explanatory Report, p. 16).

However, the applicable contractual or statutory investment restrictions (which can be very flexible) must be specified in the fund agreement of a contractual Investment Fund, the investment guidelines of a SICAV/SICAF, or the partnership agreement of an LP (article 118n et seq. PD-CISA). An L-QIF may apply the investment restrictions of supervised fund structures on an optional basis. Further specifications concerning investment restrictions could, potentially, be included in the CISO. It is strongly hoped that “hybrid” L-QIFs which invest in more than one asset class (e.g., equity and real estate) will be permitted under the CISO.

– Fund administration: The Preliminary Draft proposes – as a general rule – that an L-QIF must delegate its fund administration to a FINMA-authorized fund management company (Fondsleitung) (article 118g et seq. PD-CISA). An exception from this general requirement shall apply in case of an L-QIF in the legal form of an LP if the general partner is a bank or insurance company (article 118h(3) PD-CISA). The insertion of further exceptions from the general rule would be a desirable change from an industry perspective (e.g., in case of a self-managed SICAV or SICAF).

– Asset management: The fund administration company (or general partner in case of an LP) of an L-QIF may – but is not obliged to – delegate the asset management to (i) an asset manager of collective investments according to article 2(1) lit. c FinIA, or (ii) a foreign asset manager of collective investments if it is subject to an equivalent regulation and supervision in its domicile country and a cooperation agreement exists between FINMA and the responsible foreign authority (article 118g et seq. PD-CISA). In addition, the rules of the regulatory authorization cascade apply, i.e., the asset management may be delegated not only to asset managers of collective investments but also to financial institutions with a higher regulatory standard such as a bank, a securities house, a fund management company, or an insurance company (article 6 FinIA; Explanatory Report, p. 23). Therefore, all these types of financial institutions could benefit from launching an L-QIF (and conducting its asset management).

– Custodian bank: L-QIFs in the legal form of a contractual Investment Fund, a SICAV and a SICAF must appoint a custodian bank (Explanatory Report, p. 15). The custodian bank is authorized and supervised by FINMA and has an important (indirect) control function by way of a self-reliant review of the fund documentation (Explanatory Report, p. 15 and p. 31). More specifically, in case of a contractual Investment Fund the approval of the fund agreement (and amendments thereto) by the custodian bank are a regulatory requirement (article 118j(1) und 2 PD-CISA).

– Audit company: An L-QIF must nominate a regulatory auditor (the same as the statutory audit company; see below) (article 118i PD-CISA). By way of a regulatory audit, the audit company must determine whether the regulatory requirements of the CISA are fulfilled and will continue to be fulfilled in the foreseeable future (Explanatory Report, p. 24). In addition, the audit company must conduct an accounting audit (Explanatory Report, p. 24).

– No FINMA-approval or supervision: Similar to the Reserved Alternative Investment Fund (RAIF) in Luxemburg the L-QIF does not require an authorization or a product approval by FINMA (article 13(2) and 15(3) PD-CISA). A mere notification of the FDF by the administrator is sufficient. Thus, if the requirements of the CISA for an L-QIF are fulfilled it can be launched very quickly. Also, the L-QIF is not subject to an ongoing regulatory supervision and the related authorization and approval of ongoing changes by FINMA (Explanatory Report, p. 31).

– Investor information: The legal name (Firma) of the L-QIF must always include the designation “L-QIF” as well as the selected legal form (see section 2; article 118e(1) PD-CISA). On the first page of the fund documents as well as in advertisements, this designation must be stated (article 118e(2) lit. a PD-CISA). In addition, a disclaimer must be included that the L-QIF does not have an authorization or approval from, and is not supervised by, FINMA (article 118e(2) lit. b PD-CISA). Furthermore, special risks of alternative investments must be pointed out in the designation, in the fund documents as well as in advertisements (if applicable) (article 118n(2) PD-CISA).

4) Conclusion and Outlook

Overall, the FDF has succeeded in preparing a new and very flexible fund product. The introduction of the L-QIF represents an impactful step to increase the attractiveness of Switzerland as a fund production location and creates a business opportunity for innovative fund providers (especially, for the Swiss market). After a decade of ever massively increasing regulation in the area of financial products, the Swiss funds and asset management industry will experience a regulatory product innovation with deregulation. Qualified investors will be able to invest in a professionally managed fund vehicle with a very short time-to-market. The L-QIF may even have the potential to be considered a growth catalyst (especially, for alternative investment or crypto fund providers) in the near future.

Meanwhile, the industry has the chance to respond to the prosed new rules during the consultation process, which will end on 17 October 2019. As a next (major) step after the completion of the consultation, the revised versions of the Draft-CISA are expected to be published (and, subsequently, dealt with in Parliament). It will be exciting to see how the industry provides feedback during the consultation and to what extent further changes will be made by the Parliament. The entering into force of the new L-QIF provisions in the CISA is expected in 2021.

Sandro Abegglen (sandro.abegglen@nkf.ch)

Luca Bianchi (luca.bianchi@nkf.ch)