Structured products under FinSA

The entry in force of FinSA and the FinSO has introduced several changes to the regulation of structured products in Switzerland. Some changes appear directly in the specific rules on structured products, but most of them derive from their inclusion in the FinSA’s general framework. This article presents the new regulation of structured products as of 2020 and discusses a select handful of specific issues.

By Jeremy Bacharach1 (Reference: CapLaw-2020-22)

1) General overview

The regulation of structured products has undergone a significant makeover as of January 2020 with the entry into force of the Financial Services Act (FinSA) and the Financial Services Ordinance (FinSO). Until 2019, structured products were subject to a rather “lightweight” regulation under former article 5 of the Collective Investment Schemes Act (CISA) and former articles 3(7) and 4 of the Collective Investment Schemes Ordinance (CISO). They never truly fit within these legal texts, as they do not qualify as collective investment schemes per se — something the law explicitly recognized (see former article 5(2)(c) CISA).

As of 2020, the specific rules on structured products have been transferred to articles 70 FinSA and 96 FinSO — a more appropriate venue. Accordingly, the relevant provisions in the CISA and CISO have now been repealed. This is more than a mere relocation of the former legislation, however, as the FinSA and the FinSO have introduced several changes to the regulation of structured products. Some changes are immediately apparent, since they appear directly in the specific rules. Others are less evident — but nonetheless important — because they derive from the inclusion of structured products in the FinSA’s general framework.

It should also be noted that no change has been made to article 94(3)(a) of the Financial Market Infrastructure Act (FMIA), pursuant to which structured products are excluded from the rules regarding derivatives trading (i.e., clearing, reporting, risk mitigation, etc.).

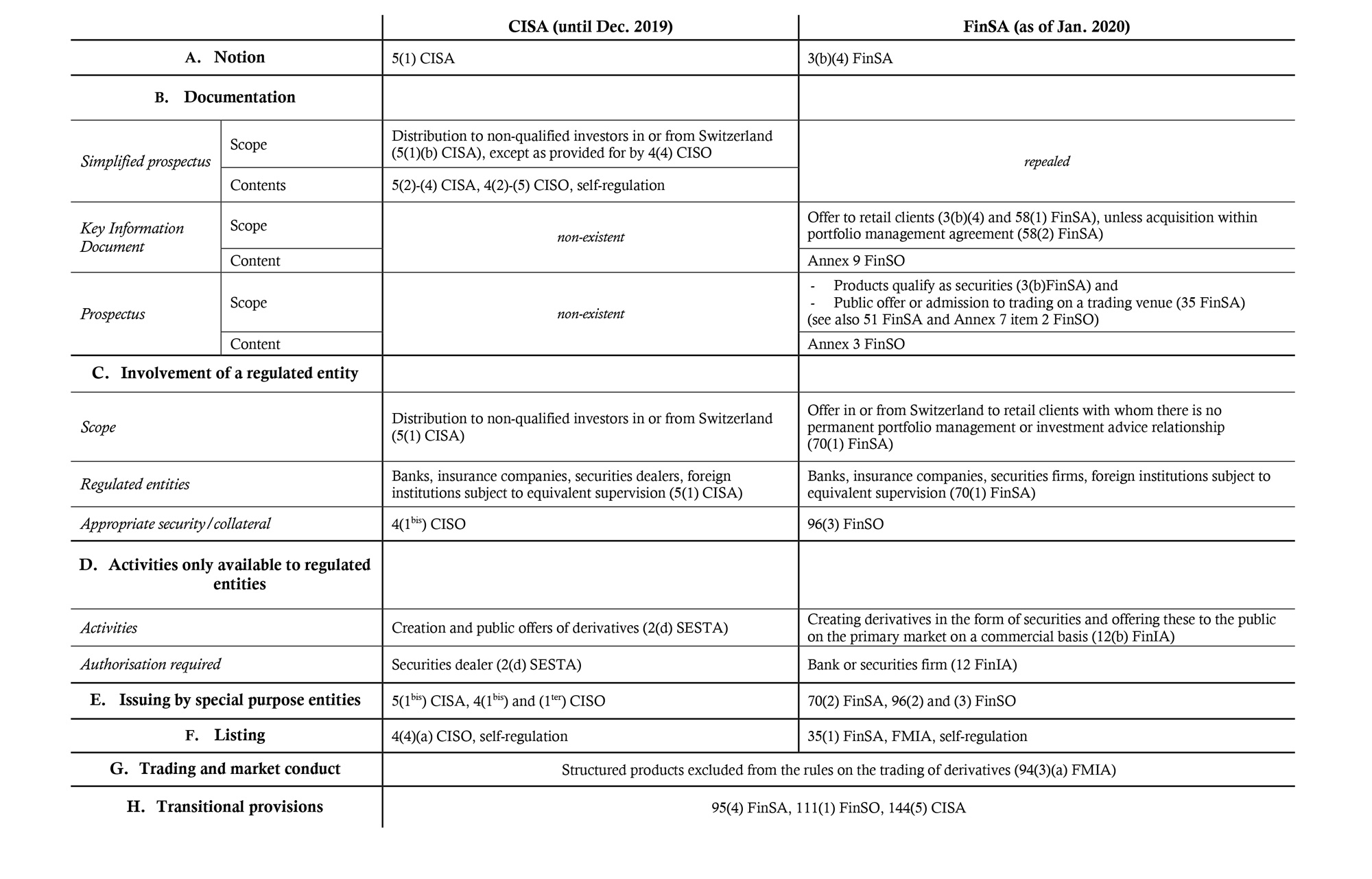

The table below summarizes the new regulation of structured products as of 2020 under the FinSA and the FinSO. A handful of more specific issues are commented thereafter.

2) Specific issues

a) Qualification as financial instrument

Structured products now qualify as financial instruments pursuant to article 3(a)(4) FinSA. As a result, the rules applicable to financial instruments, their offering, and, as the case may be, the provision of financial services are also applicable to structured products. Besides the FinSA’s general framework, articles 70 FinSA and 96 FinSO provide more specific rules on structured products. In any case, the old system, which whereby structured products were regulated specifically and on an “ad-hoc” basis, is no more.

b) Lack of definition

As was already the case under the CISA, the FinSA does not rigorously define structured products. According to article 3(a)(4) FinSA, the notion of “financial instruments” includes “structured products, i.e. capital-protected products, capped return products and certificates.” This list of examples is similar to the one that article 5 CISA used to provide. As a result, the same types of instruments are covered by this provision, such as trackers, certificates, reverse convertibles, warrants, so-called “exchange-traded products,” and others.

In case of doubt as to whether a particular product qualifies as a structured product under FinSA, it is possible to do either of the following:

– Refer to the Swiss Structured Products Association’s Swiss Derivative Map and verify whether the product falls into one of its categories (see also FinSO Annex 3, items 1.2.2 and 3.0);

– Refer to the definition provided by the European Securities and Markets Authority, which, in our opinion, generally matches the practice in Switzerland: “‘structured retail products’ [. . .] are compound financial instruments that have the characteristic of combining a base instrument (such as a note, fund or deposit) with an embedded derivative(s) that provides economic exposure to reference assets, indices or portfolios. In this form, they provide investors, at predetermined times, with pay-offs that are linked to the performance of reference assets, indices or other economic values.“2 It should be noted, however, that Swiss law does not classify structured funds and structured deposits as structured products under article 3(a)(4) FinSA but as units in collective investment schemes (article 3(a)(3) FinSA) and variable return deposits (article 3(a)(6) FinSA), respectively.

c) Duty to publish a prospectus

A notable consequence of the classification of structured products as financial instruments under article 3(a) FinSA is the duty to publish a prospectus if, cumulatively,

– the product qualifies as a security under article 3(b) FinSA, that is, instruments that are standardized and issued for the purpose of being traded en masse on the financial market.

– the product is either publicly offered or admitted to trading on a trading venue (article 35(1) FinSA).

If these conditions are met, then the prospectus should be drafted in accordance with FinSO Annex 3 (“Minimum content of the prospectus: Scheme for derivatives”). The FinSO also contains a specific alleviation in favor of structured products: pursuant to item 2 of FinSO Annex 7, prospectuses for structured products may be published before they are submitted to the reviewing body (provided that the requirements of article 51(2) FinSA are met).

d) Offers to private clients

Under the CISA, distributors of structured products to non-qualified investors were required to provide a “simplified prospectus” (former article 5(1)(b) CISA). Its contents were defined by the Swiss Bankers Association and the Swiss Structured Products Association’s “Guidelines on informing investors about structured products,” which were approved by FINMA and last updated in 2014.

The FinSA replaces the notion of “distribution to non-qualified investors” with the notion of “offer to private clients” as the trigger to a certain number of requirements. Offers are defined by article 3(g) FinSA as “any invitation to acquire a financial instrument that contains sufficient information on the terms of the offer and the financial instrument itself” (see also article 3(5) FinSO). In turn, article 4(2) FinSA defines private clients as clients who do not qualify as professional clients under article 4(3) FinSA.

Offers of structured products to retail investors have to meet the following requirements:

– First, and as a consequence of the inclusion of structured products in the FinSA’s general framework, the issuer must produce a Key Information Document (article 58 FinSA; FinSO Annex 9). This is not required if the products are acquired for clients within the scope of a portfolio management agreement (article 58(2) FinSA; article 83 FinSO).

– The products must be issued, guaranteed or secured by a regulated institution (article 70(1) FinSA; article 96(3) FinSO). This is not required if the offering is made by the clients’ portfolio managers or investment advisors (as defined in article 96(1) FinSO).

– If the issuer is a special-purpose entity (as defined in article 96(2) FinSO), the offering must take place through a regulated institution and collateral as must be guaranteed by a regulated institution (article 70(2) FinSA).

Additionally, offers or sales of structured products may also qualify as the provision of a financial service (see below).

In practice, the alleviations for offers made through portfolio managers will have two main implications.

First, it will be considerably easier for non-regulated issuers to market their product through regulated institutions such as banks, securities firms, or portfolio managers. In other words, non-regulated issuers are encouraged to interact with regulated institutions, which will in turn market the products in question to their clients and not with the end clients themselves.

Second, portfolio managers will be able to offer their own structured products to their clients, or to arrange for the issuance of ad hoc structured products for their clients by third-party issuers, in a relatively unregulated way. The reasoning is, obviously, that the duties imposed upon portfolio managers by the FinSA (see articles 6 ff. FinSA) are sufficient to safeguard the clients’ interests in this context.

e) Marketing and selling

First, the marketing of structured products is subject to the rules on advertising for financial instruments pursuant to articles 68 FinSA and 95 FinSO. In particular, it should be clearly indicated as such (article 68(1) FinSA) and must mention the relevant documentation (article 68(2) FinSA).

The marketing and selling of structured products to potential buyers directly may also qualify as a financial service under article 3(c)(1) FinSA (“acquisition or disposal of financial instruments”). Indeed, article 3(2) FinSO provides that “[t]he acquisition or disposal of financial instruments within the meaning of [3(c)(1) FinSA] is deemed to be any activity addressed directly at certain clients that is specifically aimed at the acquisition or disposal of a financial instrument.” The Federal Council’s commentary of the FinSO seems to indicate that this broad definition encompasses any and all activities that may lead a client to acquire a particular financial instrument3. We raise doubts as to whether article 3(2) FinSO – a “level 2” act – is a legally valid implementation of 3(c)(1) FinSA – a “level 1” act – with respect to the substantial alteration of the latter’s initial meaning in the ordinance. In any case, the consequences of such a broad implementation of article 3(c)(1) FinSA are not clear yet.

Should the marketing and selling of structured products be deemed a financial service under article 3(c)(1) FinSA and 3(2) FinSO, actors marketing structured products — even in the absence of an offering under article 3(g) FinSA — would have to comply with the FinSA Code of Conduct (article 7 ff. FinSA) and, as the case may be, be registered in a register of advisors (article 28 ff. FinSA). Subsequent practice will show whether this broad conception of financial services will be upheld or relaxed.

Jeremy Bacharach (jeremy.bacharach@unige.ch)

1 – The author sincerely thanks Prof. Luc Thévenoz for his thoughtful remarks and his advice as well as Prof. Rashid Bahar for his insights on some key points of this article. An earlier version of this article was first published on the website of the University of Geneva Centre for Banking and Financial law under https://cdbf.ch/1094/.

2 – European Securities and Markets Authority, Opinion: Structured Retail Products – Good practices for product governance arrangements, ESMA/2014/332, 27 March 2014, p. 3.

3 – Federal Department of Finance, Financial Services Ordinance (FinSO), Financial Institutions Ordinance (FinIO) and Supervisory Organisation Ordinance (SOO): Explanations (published in French, German and Italian), 6 November 2019, p. 19.